Equity markets churned a lot at the end of last week, especially in the US and Japan where central bank policy announcements confirmed what commentators had expected. The ensuing sharp moves made it clear that markets had not discounted any particular action; strength was followed by weakness and both markets covered as much ground upward and downward, in a day and a half as they had done in the prior week and a half.

Friday was due to be a turn day and this violence makes it hard to interpret. Was it a high that came a day early or a low that came on time? We are choosing the latter as all the other markets are behaving in a way that suggests this turn marked a dip in an existing uptrend and that the uptrend will now continue.

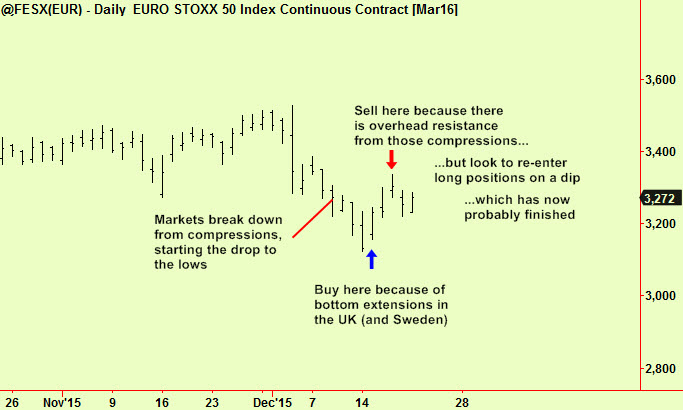

We suggested selling short the usual candidates – the Southern European equity indices – for a quick trade in the December 17th edition and that produced some profits if you were fast enough to take them. In the same edition we noted that we would re-establish the underlying long positions originally advised in the December 15th edition on a dip. The subsequent drop from Thursday’s high to Friday’s low was probably the dip we were seeking and equity prices are now free to resume their normal year-end rally. This will probably mean the trading range will continue in US markets, bounded roughly by 2000-2100 in the S&P with occasional excursions outside these limits and that European markets could do a bit better.

We stick to our usual view that the underlying dynamic caused by the existence of the Euro will continue to push Germany higher while holding back Italy, Spain, France Portugal and Greece. Accordingly while these less productive economies are chained to the highly productive Germans we will continue to recommend buying Germany when it is time to be long and selling some of the others when it is time to be short, in Europe.

We remain sidelined in the US and would continue to trade the range, from both sides.

The recent story is best told in a chart – here we paste a summary of the advice on to a Eurostoxx futures chart:

More soon on bonds, which are re-compressing.