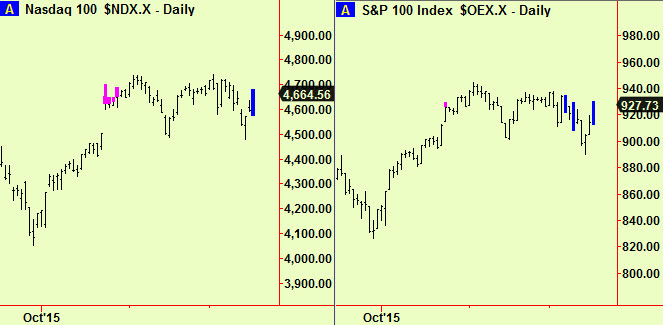

There were more daily-scale compressions in US equity indices yesterday, reinforcing the point that US markets remain range-bound and that the range may still be traded from both sides. The Fed decision to raise rates in line with expectations might provoke a break of the range but we cannot tell which way. If it is upward then there is still the possibility that a bubble may inflate as this modest monetary tightening comes too late to reign in the bull market. We wait.

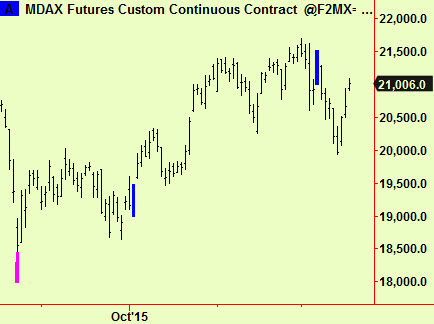

European stock have rallied sharply, especially our favourite ‘long candidate’ the DAX. Prices are now in resistance from old compressions that formed and broke downward just over a week ago. One example will do to show the situation – the MDAX index of German secondary stocks. This means that there may be some reversal of this up-move. from hereabouts.

We have taken profits on European and Japanese longs today but may look to re-establish them on a dip. Brave souls could short-sell the usual ‘short candidates’ of France, Italy and Spain – perhaps France being the best one – for a short-duration trade.

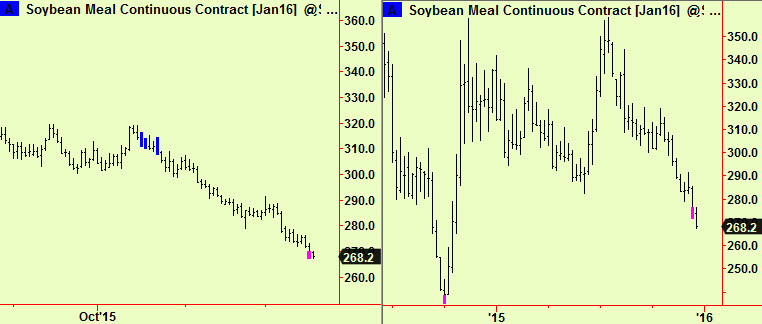

Elsewhere, soya meal futures made a daily-scale bottom extension yesterday to complement the weekly-scale version seen last week. Prices have weakened a bit since that first signal but this still looks like a good ‘long’ position.

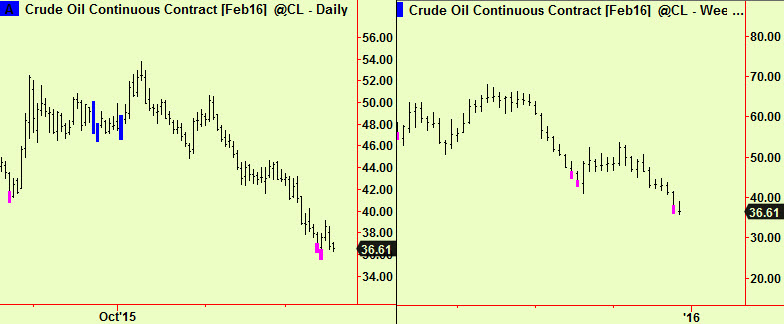

There have been bottom extensions in energy markets too, but these are failing to provoke much of a bounce (yet). The reason is probably that energy is not a true ‘free market’ and is under much international government influence – the Saudi Arabians and their Gulf allies are pushing out a lot of crude to try and maintain market dominance and this is tough to fight. Still, we do expect a bounce and are trading from the long side. Charts: