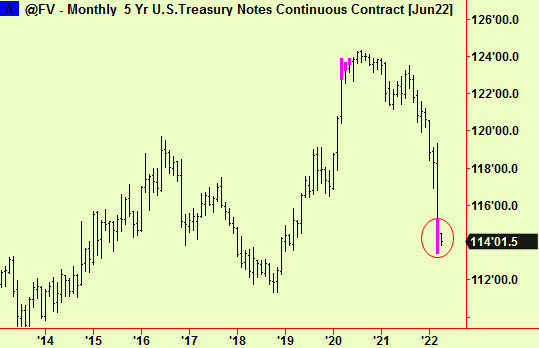

There has been little to say, so we have stayed silent since the last edition on March 23rd. Since then, month-end has come and gone and we have some monthly-scale signals to report, later in this edition and in editions to come. Meanwhile, that last edition pointed out two extension signals that occurred in markets that have had strong moves – the Yen and US 5 Year T-notes. These two were part of the group of markets that had reacted sharply to Putin’s war on Ukraine so we surmised that the current phase might be ending (although it is thin evidence) as markets might relax a bit over the Ukrainian horror. We advised taking some profits and waiting for a while. Here’s an update, firstly to the 5 Year and other fixed-interest markets:

We have been proclaiming that bonds are in a bear market for about a year and we expected that any rally would provide a new chance to sell. Now we have new evidence that a more important low point may have been reached. There has also been a monthly-scale bottom extension in the 5 Year:

As the caption cautions, monthly-scale charts are a poor timing tool. We already have daily-scale signals however, so we now advise buying US bonds across the curve.

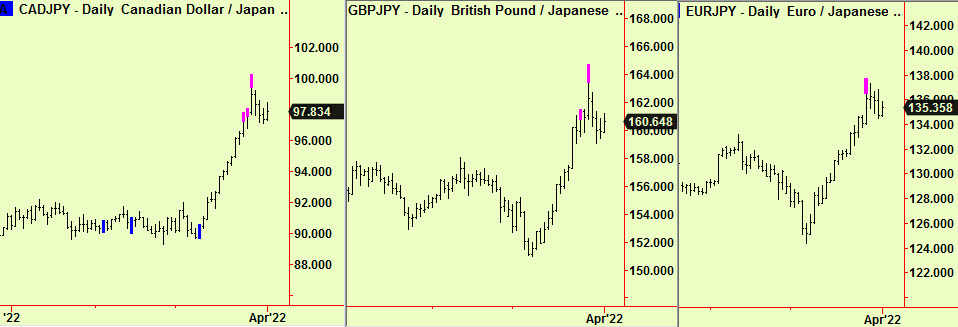

The other signal that caused us to think that the market weather might change was in the Yen. We showed $-Yen as our example but it had extended against several other currencies too. Here are more:

This seems to argue that the immediate level of market panic has now abated. This seems obvious today, after Russia’s evident military difficulties but this was almost ten days ago, when the invasion seemed to be a greater success for Putin than it does now. The relative ‘relaxation’ has more time left, as these signals won’t expire for another week. Meanwhile, on the subject of currencies, there has been a new daily-scale compression in the $ index, that is (so far) breaking upward today:

We don’t usually advise taking a position as soon as a price ‘breaks’ either way from a compression, because of all the different possible outcomes. In this case, it looks as though we are seeing a ‘good clean break’ early on, so we would buy this index. We will comment further as events unfold as ths might prove to be a very short-term trade!

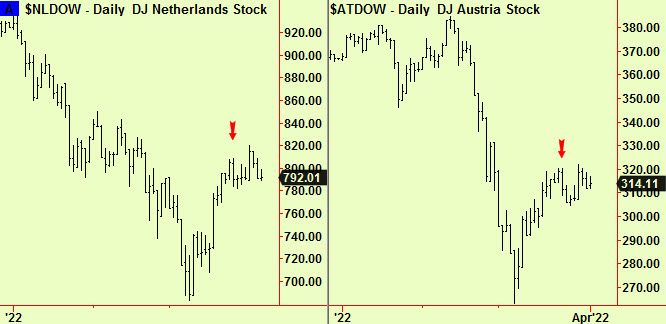

In the last edition we also advised trying a short in selected European indices, contrary to what we think is the main uptrend – of course, if you don’t think short-term, you may use these contra-trend trades as opportunities to sit and wait for a few weeks before joining the main trend. We suggested picking those that had rallied the weakest, which is our usual policy when picking shorts. Here is an update for the first two on our list. The advice was based on markets ‘bumping up against’ resistance from old compressions and we generally expect that prices will fall away quite quickly from such ‘retests’. These haven’t fallen much (yet) so we would tighten stops and think about covering in the next few trading days if there is no sign of weakness:

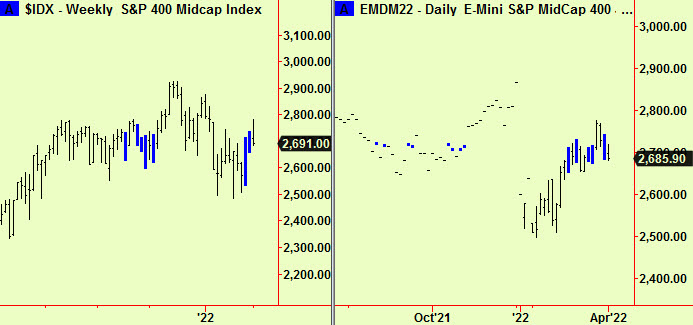

In US stocks we remain sidelined. The reason we gave is that some mid-cap indices are compressing at both daily and weekly scales and these are ‘knife-edge’ moments. We don’t have any way of knowing which way prices will break from compressions, so we wait. The two we chose to illustrate this condition are still compressing by the way, so here is an update. The daily-scale version seems to be (just about) breaking downward so far today, but there is still two and a half hours of the trading day to go. We wait.

Lastly, Soy. We mentioned in the last edition that we were worried about Soy markets at these high prices. The Ukraine grows massive mounts of Wheat, Corn and Sunflowers but few Soybeans. Any weakness in grains would probably show up in Soybeans first and so it has been. There was a daily-scale compression in Bean futures on Monday, a break down on Tuesday, a rally to ‘retest’ on Wednesday and resumed weakness yesterday and today. This has more to drop, so sell now and on any rally:

All signals generated by software produced by our friends at Parallax Financial Research www.pfr.com