Equity markets are surprisingly steady, considering the see-sawing military tension on three sides of poor Ukraine. Wars have a habit of spreading, so if this one starts, it is not guaranteed that it would remain confined to that sad place. Much is written about the cunning of Russia’s leader and his ability to manipulate the leaders of democracies but we have noticed a tendency for him to overplay his hand in recent years. He and the whole Russian governing culture are in thrall to thoughts of conspiracy and the intelligence services of the Western countries have done a good job of exposing his moves before he makes them, so revealing his nonsense before it has time to do much harm. Markets seem to think that this reduces the likelihood of a large conflict and perhaps that is right. We rely on our analysis of crowd dynamics, which can obviously be undone by events but even then we can offer some guidance.

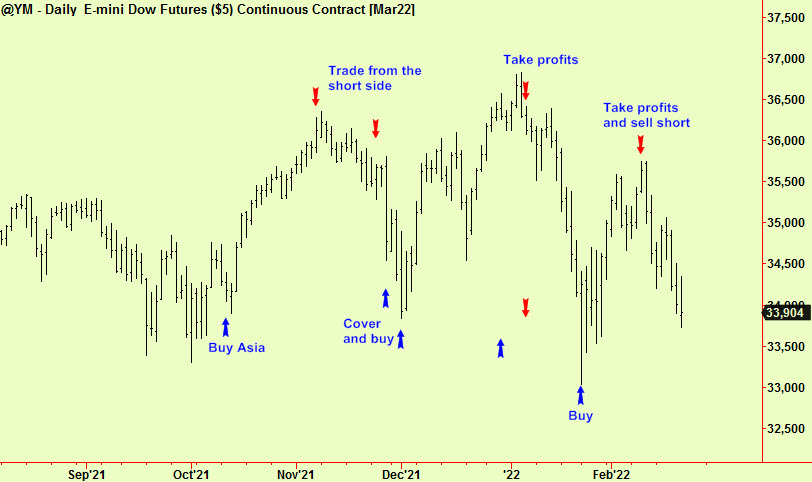

Our posture over the last year has been to forecast a trading range in many world equity markets and to try and pick the index highs and lows within those ranges and also to identify the inevitable sector rotations that occur, especially in such ranges. We stopped that in October last year and sat out the final three-week rally in the US, choosing instead to advise long positions in Asia, which performed exactly the same as the US. Here is a summary of all we have said since then, pasted on to a chart of Dow futures:

We turned bearish of US indices in the November 5th edition but advised trading from the short side, not taking a strategic ‘sell a hold’ bear position. We repeated that advice on November 23rd but advised covering and taking long positions on the sharp weakness that had occurred by the 26th November, adding long advice in other equity markets that day and on December 1st. All worked well except Singapore. We advised tightening stops on longs through last year’s ‘Santa rally’ and these were elected in the US as the markets dropped from new highs on January 6th, pointing out that there was potentially a large hole under the market.

We advised buying European indices on January 12th, inserting a bad pun about notes. There was no advice yet on US indices, so we assumed readers would be flat. This changed to a bearish view on the 24th January, after a sharp drop although we cautioned not to sell short just yet. In fact, we saw a bounce coming and advised ‘buying for the bounce’.

This advice reversed on February 8th when we advised taking profits and selling US indices short if prices rose about 2% more. They did this the next day and we have held to that short view since then.

Now there are some reasons to moderate that bearish view There was a weekly-scale bottom extension in an Internet stock index we follow three weeks ago and that extension has several more weeks of shelf life. In addition the much-watched Dow transport index has dropped back to where we expect support from an old weekly-scale compression:

Nether of these is a ‘major index’ so the best clue as to what happens next might come from the UK. The FTSE index has been largely unmoved by the soaring and plunging going on across the Atlantic and it has just compressed. This signal is only at a daily scale, but it offers a chance to tighten stops on short positions in any market with which it is correlated and even reverse into longs IF it breaks upward. The high of that day was 7553, the low 7441.5:

All signals generated by software produced by our friends at Parallax Financial Research www.pfr.com