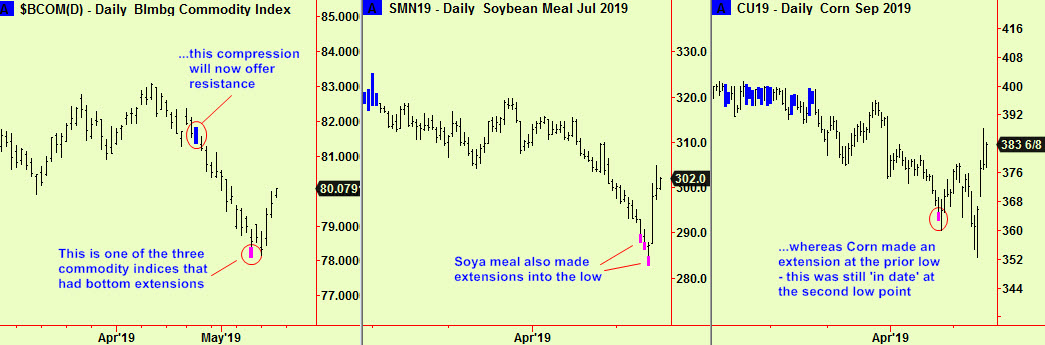

Grains have rallied sharply in the last few sessions after the scattering of bottom extension signals that we have been reporting. This new rally probably marks that end of the bear phase that has gripped many crop commodities in recent months and quarters and we have been pointing out that conditions were ideal for exactly such a change of state. Some updates, starting with a commodity index:

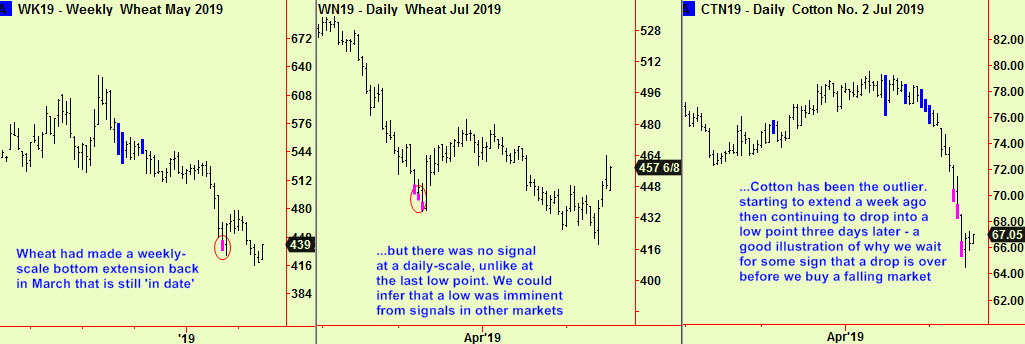

Wheat also rallied sharply, but we had to relay on a weekly-scale bottom extension to anticipate the low before the rally, as there was no daily signal in any of the delivery months. Luckily there was enough evidence from other grains and from those commodity indices. Cotton also extended but the price drop then accelerated for two more days – it’s still dangerous to ‘catch a falling knife’ even when there are bottom extensions:

To conclude – it seems highly probable that the most recent bear ‘leg’ in grains and some other crop commodities is now over. This most recent weakness was of course caused by fears that the US and China would not resolve their differences and so the export markets for US crops would diminish or disappear. Those fears are still real and the spat between presidents Trump and Xi seems to have intensified, not lessened. That has not impeded the sharp rally of the last few days, which should not be surprising to seasoned observers of markets. Some observations:

- China will buy its grains from somewhere, even if it is not the US. This means that the world supply and demand for grains will be unaltered – trade routes will shift, that is all

- The world population is growing at the fastest rate in human history, in actual numbers of new people per year. As we have pointed out many times before, this annual growth rate of a little over 1% translates into 80 million more mouths to feed every 12 months. This is equivalent to a new Greece every six weeks or a new US every four years. It would take 16.5 years to breed a new India, 17.5 to make a new China. Staggering!

- Against this, harvests are also growing by about the same amount, caused by improvements in agricultural practice and the extra CO2 now circulating in the atmosphere (it’s the basic plant food, after all) from humanity’s activities. The chance of a dip in production caused by poor weather or other problems is 100 times more likely than a dip in population growth. El Nino is lot more common than plague or nuclear war so we have been advising for some time that crop commodity prices are ‘bumping along the bottom’.

- That process continues and we believe that the most recent weakness that ended with the last few days’ rally was just another ‘stab downward’ within that greater tendency. Rallies come next and we will try to navigate them as best we can, as usual. Don’t be surprised if they are large.

Stocks have stopped falling in the last few days and there are some rallies going on, as we wrote was likely in the last edition. There have been some more bottom extensions in the last few days, which make us think that these rallies will persist a while longer. We include the signal from Indonesia here, for the usual reason that signals can sometimes occur in less-examined markets that have predictive power for their larger neighbours.

These three have fallen by roughly 7%, 6% and 11% since the present weakness began in the first few days of May, compared with a drop of 4% in the S&P in the same period and one of 8 or 9% in China, depending on what index you choose. This seems to bear out President Trump’s assertion that the US is less troubled by the consequences of a trade war than its opponents (not just China, let’s not forget). This is apparently confirmed by an IMF study that projects a reduction in Chinese GDP by a median of 1% if 25% tariffs were imposed on all trade between China and the US but a corresponding drop in America’s of only 0.45%.

These numbers will serve to encourage Mr Trump in his determination to prosecute the present trade war and perhaps to widen its scope to even more European sectors. What the numbers don’t (and can’t) show is the cumulative effect of several repetitions of the negative feedback loop that this sets in motion. This is our field of study and it seems likely to us that the damage would be much greater were this to persist.

Now that Agricultural commodities and equities seem to be following our script well, we will turn to bonds and currencies in the next edition.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com