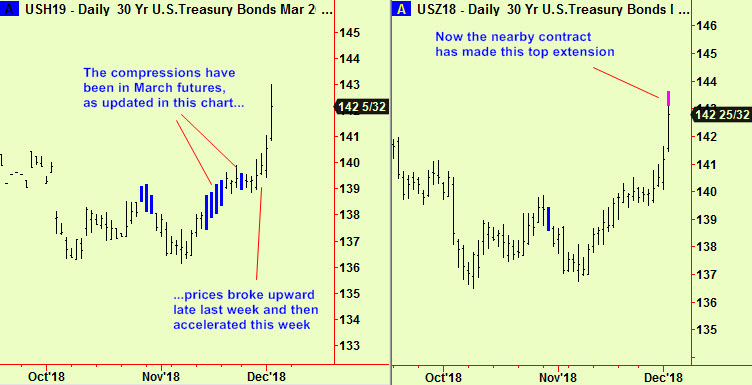

The short-covering-and-then-drop in stocks yesterday produced another squeeze, in various bonds. The US 30-year had already moved up from a compression that we pointed out in the November 28th edition and now that move has produced an extension:

We had suspected that the break out of this compression would be downward, but that’s the problem with compressions – they are moments of maximum uncertainty among the crowd and are inherently unpredictable. Not for the first time, it is worth noting that we should always wait for the start of a move out of a compression before following it. Trying to guess which way it will break is fraught with difficulty. This one broke up.

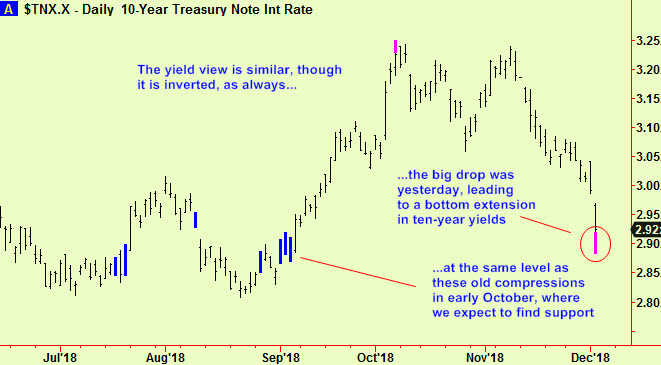

The yield picture is similar. There are no signals in the 30-year but the 10-year note yield has extended. This occurs at a place where we would expect support from old compressions, as usual:

This means that we should now actively look for places to sell US bonds and notes. The only caveat is the usual one that applies to all top extensions, which is that they often start the process of turning a market from up-to-down rather than marking the actual turn itself. The risk of selling here is greatly reduced but there is no guarantee that the markets will simply drop – they may need to ‘make a top’ which can take a while. There is always a chance that markets will make a ‘spike top’ here but they are rare, so we will wait a bit to attack the US market.

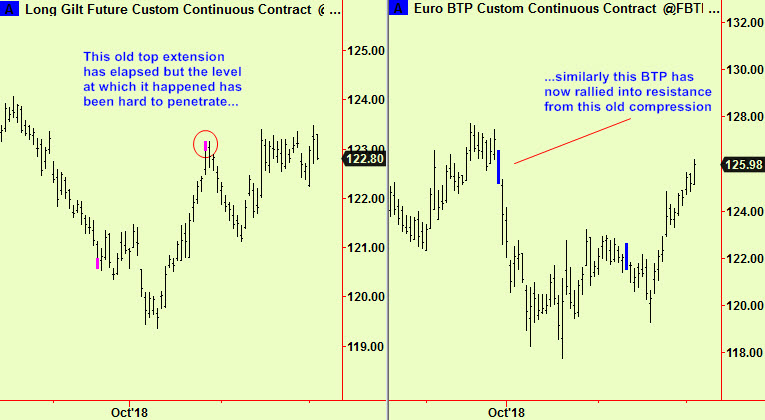

It may be better to look elsewhere for promising immediate short-sales candidates. There have been no equivalent top extension signals in the European government bond markets, even though they have rallied. Bunds continue to surge higher, as Germany at least can be relied on to pay its debts. The yield on the entire German curve as far out as 7 years is below zero, which has been the case for so long that people no longer see how strange it is. Even the German 30 year Bund has a yield of merely 1%. Some of this is due to the distorting effect of there being ‘one big buyer’ in the form of the ECB trying to inject money into the system with its multi-year purchase scheme. Yet more is due to the other ECB action in holding Euro deposit rates at negative 40 basis points but a third reason is that Germany alone is thought able to pay its debts no matter what may happen, so investment sheep flock in. This argument does not apply to France where the national debt is approaching 100% of GDP, compared to Germany’s (still strangely high) 68% but in France the yield is also negative out as far as five years and is only 1.6% at the 30-year mark. Even odder when considered calmly…

In the meantime Italy’s debt is 132% of GDP while the UK’s is around 86%, depending on how you count it. All these are high, as is the ratio in the US which hovers just above 100%. The difference between the US/UK and the Eurozone countries is that the former still have their own monetary authorities while the latter have pooled their efforts under the ECB, yet without granting full authority to mix the finances of the member countries fully together. In other words, one European country could default while the others stand by and let it happen. This is thought unlikely but it is the logical conclusion of a lack of full monetary union. That is why Italy’s government debt has a positive yield from the 6 month point, rising to almost 4% from 20 years and further forward. Nonetheless, even Italy’s BTPs have risen in price lately and are now high enough to consider selling again. The other candidate is UK Gilts which are always ‘in play’ because of the continued shenanigans of Brexit. Charts:

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com