US stocks have held support, as we suggested was most likely in the November 14th edition, even though the Nasdaq did make slight new yearly lows. We also warned in the same edition that such slight new lows were possible and now we feel that our view of a longer-term trading range is valid for a while longer – perhaps even a long while. Ranges are often erratic and we continue to watch for new signals that may offer opportunities to trade within the confines of this one but there is nothing new to report yet. It is worth repeating our often written advice that successful trading in a range requires taking profits, as they become available. This may be stating the obvious but one of the characteristics of markets is that sentiment becomes extremely bearish at the bottom end of a range and conversely bullish at the upper end. It is difficult to counter this, even for experienced traders so it is worth saying often.

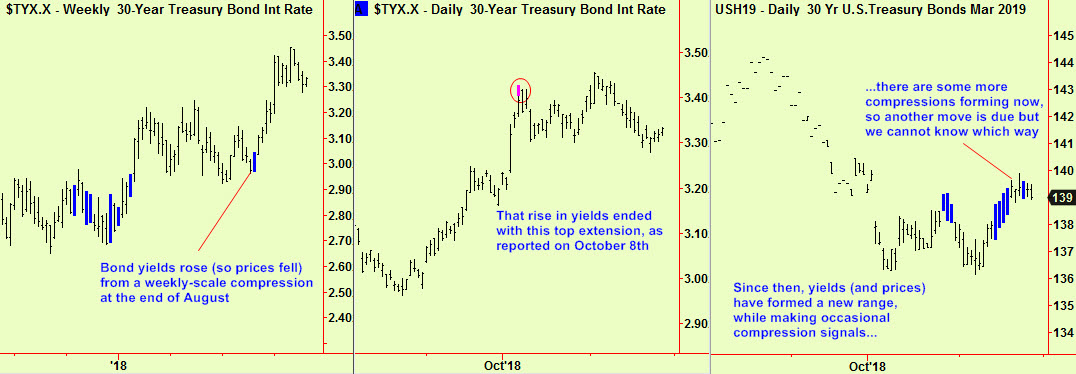

The US bond market has been range-trading for almost two months. Here is the recent history of our view, in three charts:

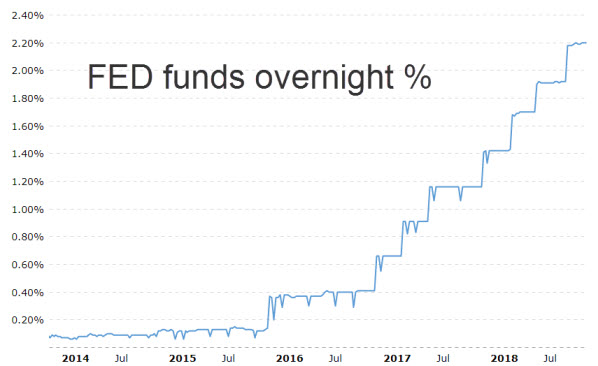

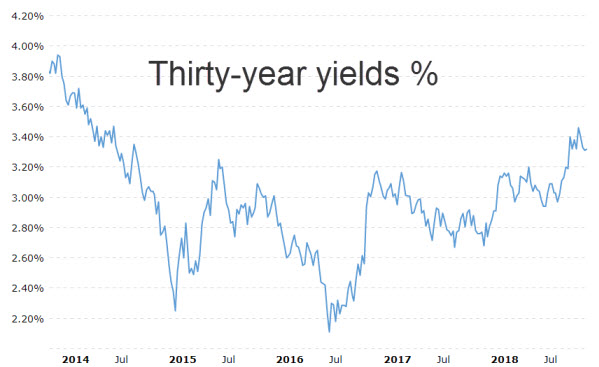

The underlying trend is still for yields to rise, as the US economy continues strong and the Federal Reserve does its mandated task by raising short-term interest rates (slowly, for now). The timing of such rises is always a matter for great speculation and we have no expertise in this so will leave it to others. We would point out the lack of correlation between moves in rates under the Fed’s control and those of bonds. Here is are two charts that update a view that we first published in the August 21st edition, showing the Federal reserve overnight rate and then the 30-year bond yield:

From which it can be seen that there has been very little connection between these two rates, even though many analysts and traders think of them as strongly linked. This means that the bond market can go either way, even when there is a strong trend for short-term rates to rise, as now.

Nonetheless, we suspect that there is an uptrend in the thirty-year bond yield too, caused mostly by the weight of new bond issuance to ‘plug the gap’ between decreased tax revenues now and increased tax revenues from increased growth (if that happens) later. This will press down on bond prices (pushing yields up) so unusually for us, we have a slight preference to sell bonds even though they are compressed. All compressions mark moments of complete confusion among participants and so it is still wise to wait for some signs that the market is weakening before selling, as indecision transforms into the beginnings of a consensus. If you see signs of that weakness starting, sell quickly.

There is nothing similar to report in European bond markets where we have had no signals for many weeks. They are stuck in the firm grip of the European Central Bank’s bond buying program, which may conceivably even be extended beyond its end-date as Eurozone economies are seen to weaken. We warned of this pending weakness in the March 7th edition, borrowing from Simon Ward’s excellent work on money supply at Janus Henderson.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com