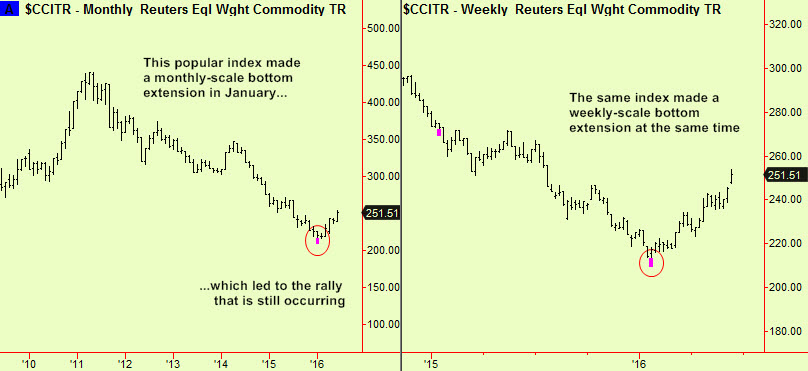

There has been a broad rally in commodities since early in the year and now there is reason to think that it will end hereabouts. The 5-year commodity price drop ended and this rally immediately started in late January with monthly and weekly-scale bottom extensions in an equal-weight index that we follow:

Now, five months later we are seeing weekly-scale top extensions in related indices (related because these are all calculated with equal weighting for each component):

Top extensions often mark the start of a ‘topping process’ instead of an actual high point but we are more interested in the individual components of these indices as they can be traded. Accordingly, we will continue to look for commodities to sell short as the whole sector pauses in its rally and probably starts a decline. The magnitude of any weakness that results will probably not be severe as prices for many commodities are already quite cheap by the standards of the last decade but drops of 10-20% are still worth catching.

We already have outstanding short recommendations in copper, sugar and natural gas, with one remaining long recommendation in cocoa. A long trade in wheat ‘timed out’ a few days ago. We are watch the whole sector and will advise further soon.

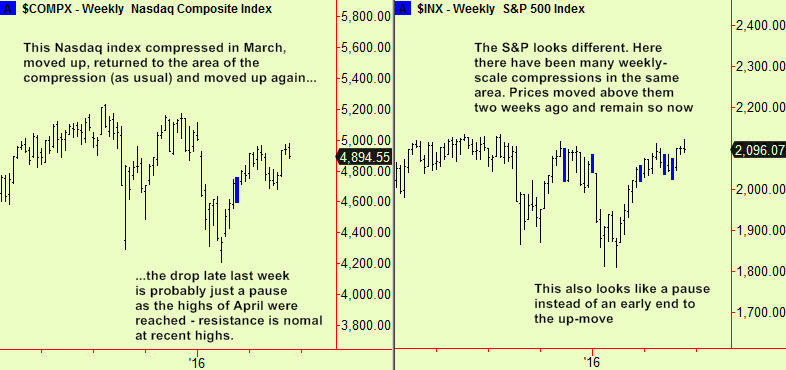

Meanwhile, equity markets dropped on Friday, quite hard in Europe. Our long campaign was bruised by this but the reasons to be long of US markets are still valid. To summarise, the breaks above compressions that occurred in recent weeks are still valid and this looks like a dip, not an end to the ‘leg up’ that we expect:

The European picture is more mixed, probably because the longer-term earning trend in European stocks has been poor and there are worries about geopolitics as particularly affecting the EU in general and the Eurozone in particular. The Brexit debate is another worry – it is inconceivable to the Euro-oligarchy that these difficult Brits can’t see the advantages of paternalistic government by well-meaning bureaucrats. Well, we don’t like it and the vote on June 23rd may show that.

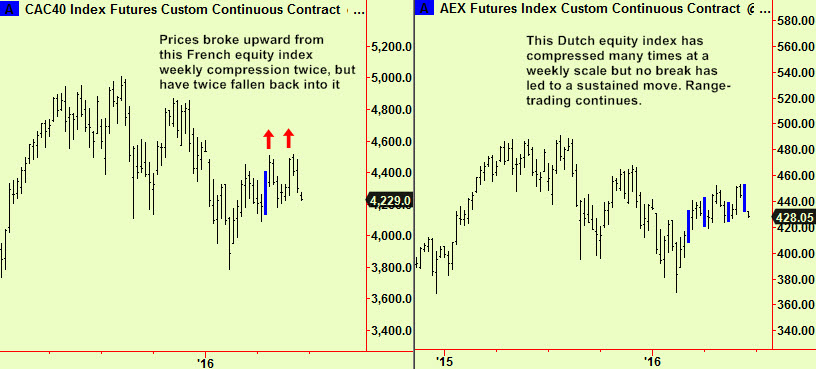

There have been multiple weekly-scale compressions in European equity indices too, but values have not made a clear break upward from them. Apparent breaks have stalled, as seen in this French example. The Dutch chart is typical of some others that have repeatedly compressed:

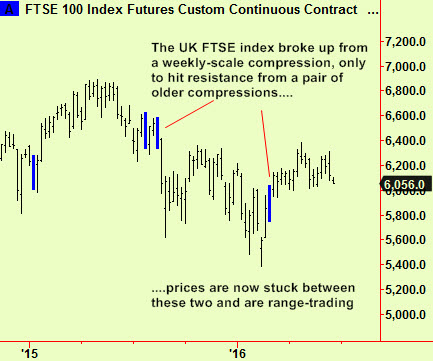

Lastly, the UK where the equity market and the currency are both moving with every lurch in the Brexit opinion polls. The FTSE has probably more potential for a rally than the mainland European indices as the fund management world is notably underweight in it. The apparent break upward from a weekly compression occurred in February but the market has simply range-traded just above that compression ever since. There are two old compressions that are providing resistance at the high end of the range and the market is stuck.

All this means that the prospects for US equities remain brighter than for Europe, as has been the case for some time. We remain bullish about the US and are cautiously bullish about Europe too but restrained by the lack of any clear upward break. If that break should eventually occur, there is a lot of headroom for a good rally but equity markets throughout the whole continent are still stuck in longer-term compressions. As in any compressed situation the break could be in either direction so we are playing defensively here, trying to keep long while not risking much.