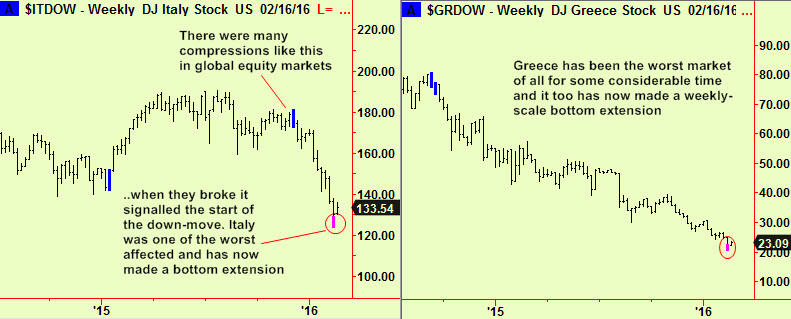

There were a series of compressions in equity markets into the end of last year which broke downwards, leading to the weakness that has caused so much fear in 2016. These compressions were at a weekly scale and so should last for about three months or until superseded by other signals. Compressions typically occur at the start of market moves which then go on to end with extensions. Compressions signify confusion and doubt whereas extensions mean agreement and uniformity of emotion – fear as the end of a price drop nears or exuberance as the end of a bull move approaches.

We have just seen the first weekly-scale bottom extensions in Equity indices, in Southern Europe. Italy and Greece have both been hit hard in the recent sell-off and had already made daily-scale bottom extensions, as reported in the February 10th edition. Now they have made these weekly signals too:

We have been advising a more constructive approach to equities for a little while, so you may now have long positions in several indices in the US and Europe. These new signals mean that we might see a better bounce than the bear market rally that we had been expecting. In fact it is possible that the drop is all over – we will reserve judgement on this for a while longer.

We analyse the mood of the market and other aspects of it that are driven by the crowd’s behaviour. Mostly we do this by using lots of different strings of prices and looking for the tell-tale fluctuations that show up in our analysis of those strings. This reveals the ebb and flow of mood and it works because the mood of the trading crowd is affected by price movement more than by anything else and the crowd’s behaviour is then determined mostly by that mood. This is an example of feedback and we are merely using modern methods to measure the same old thing that canny market observers have always watched – looking for moments when the crowd is overly pessimistic or unduly optimistic.

There are other, older ways to gauge the same thing and one is to look across at other markets for signs of oddity. Recently, there has been a flight into assets that are regarded as a ‘haven’ in times of trouble. Gold is the most obvious of these and when it goes up in times of worry it is just a normal part of the emotional swings of market life. What is not normal is the current rush into government bonds. It is well-known that government indebtedness is at very high levels in most parts of the world and this is only supportable because of the ultra-low interest rate environment. Servicing these giant debts (meeting interest payments and re-financing bonds as they fall due) is easier as yields stay low, but the outstanding amounts are extraordinarily high and still growing.

Worst among the many culprits is Japan, whose national debt is the largest by far of all the many deeply indebted countries in proportion to its economy and the debt is un-repayable in any foreseeable circumstance. Ignoring this, buyers have flooded into Japanese Government Bonds (JGBs) with such enthusiasm that all the debt out to the ten-year mark now returns less than investors are paying for it. This is presumably the latest form of ‘momentum investing’ where an uptrend assumes sacred status among investors who assume it will continue forever. QE caused the uptrend and now it seems to have become a totem.

We are not saying that this is the time to sell JGBs short, although it may be. Instead we point to this madness as an example of the extreme fear and apprehension that has apparently gripped international markets to such an extent that money is flooding into an asset that has no prospect of a positive return and may even turn out to be worthless.

This level of fear is typical of market bottoms. We have advised buying stocks, selling US T-notes, selling Yen and selling gold. The gold trade was premature and we are waiting to re-visit that but the others still stand.