US and European equity markets are trading in tight ranges near the highs of broader ranges. We have recently advised short-selling some US equity sectors and the Southern European indices (Spain, Italy and France, which are our usual short choices) based on a turn that was due late last week. There are also some older weekly-scale compressions looming above market levels that will offer resistance and which are ‘weighing down’ on prices in the medium and longer-term. These make it likely that the present broad ranges will continue, or even eventually break down. Here are examples from the US and UK, showing those compressions to be quite close overhead:

The turn day came and went last week apparently without turning the prior little uptrend into a downtrend, unless the turn came very late. It seems instead to have turned the near-term trend from upwards to sideways and we now wait for the next one which spans the upcoming weekend 23rd/26th October. Accordingly we are reviewing this outstanding short recommendation to see if it can be abandoned, perhaps to try again later. For now we wait and will advise very soon – stay short in the meantime as any downward lurch hereabouts will probably signal the start of something bigger.

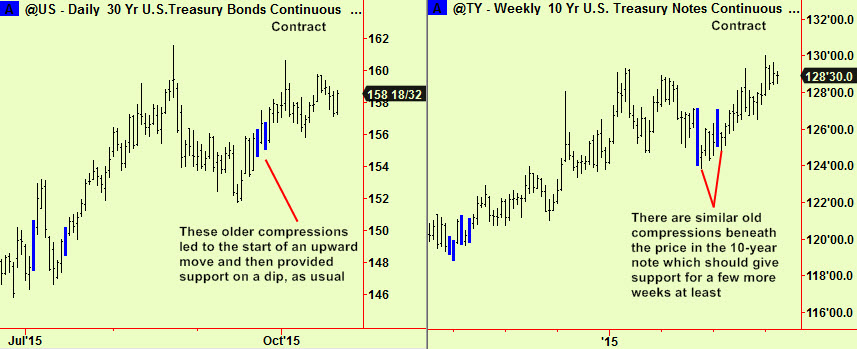

Bonds have also been zigzagging in a fairly tight range in a similar situation but here the older compressions are just below the market and have been providing support on dips. This will continue and so we are content to stick to our outstanding ‘be long bonds’ advice. There are compressions at a daily scale in bonds but also at a weekly scale in ten-year notes – these are still ‘in date’ so we expect to hold the position for a while longer, lacking other developments.

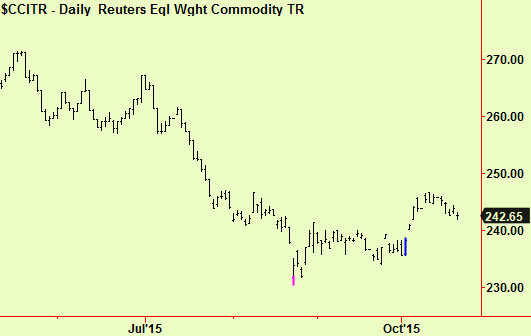

Commodities are diverging from one another a bit. The main index that we follow made some daily-scale compressions (the blue bar, below) and moved up. It is now drifting downward in what we assume to be a market reaction that will probably lead to some more strength. There will be support at the compression level, as usual:

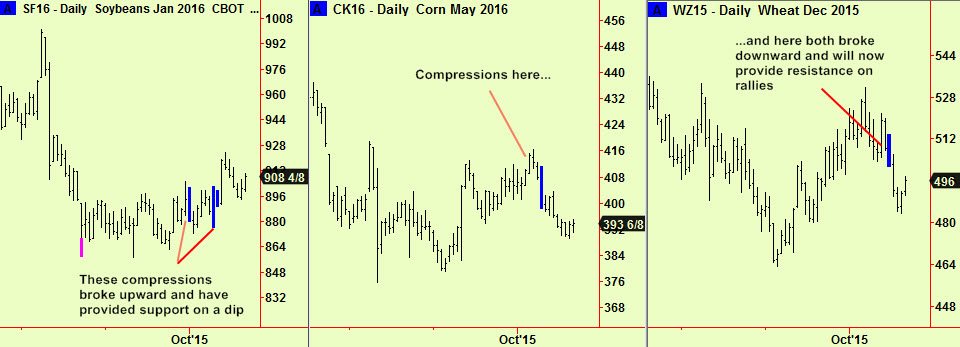

Within the grain complex, soya has been strong after compressions broke upward but wheat and corn have both compressed and fallen. This has led us to advise buying soya beans (we may also advise buying soya meal before the end of this campaign) and we would sell corn and wheat short if they approach these compressed levels – wheat is already there.

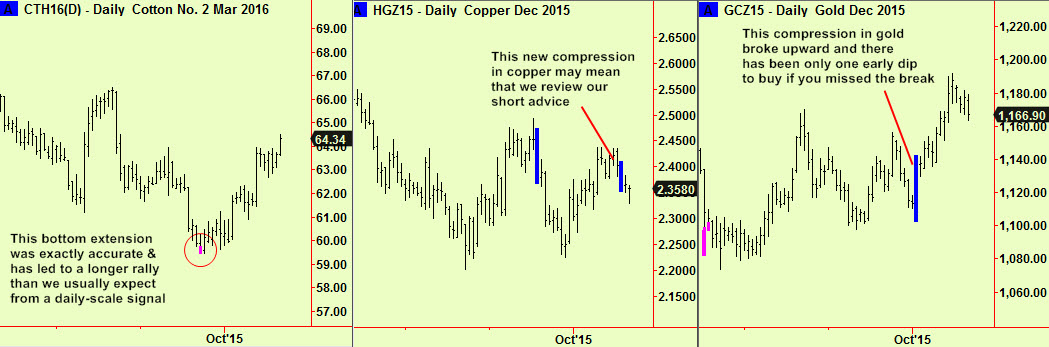

Cotton has also been strong and we ‘timed out’ of long positions too soon it seems. Copper broke down from one compression and has now formed another, which may mean that we have to review our short posture if this new compression breaks up. Crude (not shown) also pushed down below a compression reported in the October 13th edition and will now probably resume its long-term decline. Gold compressed and started to move up, dipping once after three days to re-test the compressed levels – that was the only chance to buy if you missed the break. Sugar (not shown) has traded sideways since we advised short-selling early last week.

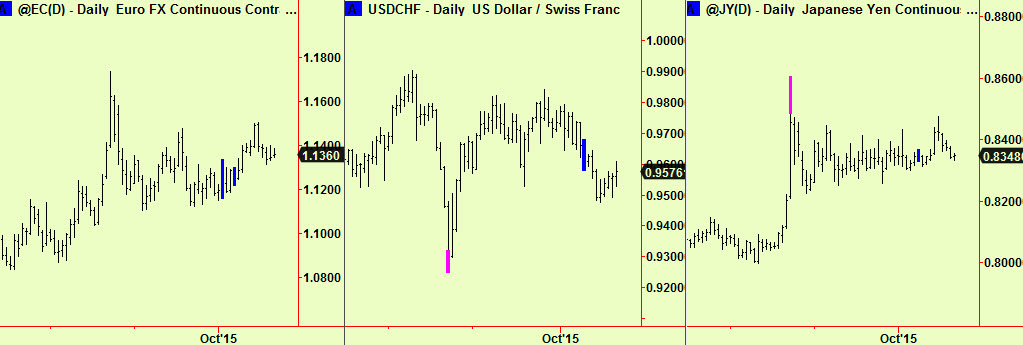

Currencies have continued to trade in slightly wider ranges than in September. We have three outstanding recommendations, each of which involves selling the $ – against the €uro, the Swiss Franc and the Yen. The €uro and Swiss trades are basically the same trade because the picture is so similar – the first chart shows the €uro futures but the second shows the $/Swiss Franc spot rate which is why it looks ‘upside down’. Compressions formed and broke in the direction of a weaker $ in both. The same is true of the Yen, but this Yen trade doesn’t look so attractive now – a ‘return to compression’ should be followed by a quick resumption of the trend in the original direction of the break and that is not happening here.

Our model portfolio did not buy the Yen for fear of over-concentration of risk and we no longer advise doing so. The same criticism could be made about the Euro and Swiss trades too – they have not briskly resumed their early trends, so we would exit here to ‘scratch’ the trades.