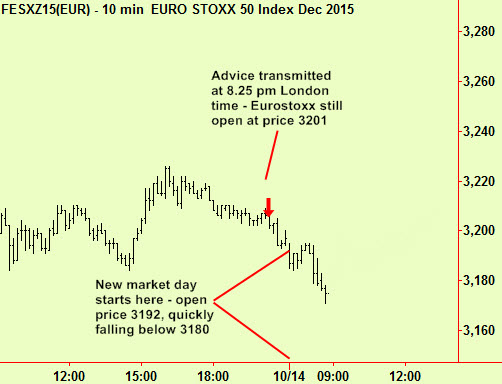

The advice ‘sell stocks short’ given in yesterdays edition at 8.25 pm included a list of markets that we considered suitable candidates to sell, including two European indices that were closed for trading at that moment. These current ranging market conditions lead to many sudden changes of direction and ‘gaps’ in price between closing and opening levels, meaning that prices might move overnight before the trade can be adopted, so how to deal with this?

We borrow a simple technique from the history of trading in Eurodollar futures strips called ‘stacking*’. Here, if the market won’t allow you to trade what you want, then pick a related market and trade that instead. Later, when your desired market allows you access, then switch from the one you are in to the one you want at a time of your choice. In this case, the suggested markets that were closed were Spain and Italy – two of our usual candidates in Europe when selling short. The Swiss, Eurostoxx, French CAC and German Dax futures were all still open, as was the FTSE, so there were several European stock index futures market from which to choose. The most suitable of these to use as a proxy for our two closed markets is the Eurostoxx, as it is the most liquid and correlates well with the Southern Europeans much of the time.

In order to take the place of both short positions in Spain and Italy it would be necessary to sell the equivalent amount of Eurostoxx futures, adjusted for volatility. The Eurostoxx is a bit more volatile than the Spanish or Italian Indices at 2.4% daily vs 2.2% and 2.1% so the face value of the total contracts needed would be reduced a little – we use the 25-day volatility for this calculation.

Prices for the Spanish and Italian indices opened lower this morning as did the Eurostoxx too – all by about the same amount. During the early part of the day, the short positions taken in the Eurostoxx can be profitably covered and simultaneously replaced with positions in these other markets, removing the extra risk of selling into weakness to establish the positions.

*The term ‘Stacking’ comes from the practice adopted to mitigate the lack of liquidity in distant-delivery Eurodollar futures when trying to buy or sell a ‘strip’ of futures to hedge a bond. The market may quote prices for each delivery up to ten years forward but there is often no real bid or offer for the far distant contracts, so trying to hedge a ten-year note with forty equal short sales of each quarterly delivery would be impossible without getting terrible ‘fills’ on those contracts for years 8, 9 and 10. Instead, the practice developed of ‘stacking’ all the quantity needed for the distant months in a nearer but liquid delivery, say 6 years forward and then gradually moving this large concentrated position forward over time. This is not a perfect hedge as it fails to capture wiggles in the far away part of the yield curve but it does hedge adequately against parallel shifts in the curve – these haven’t happened in recent years but will no doubt occur again.