We have been favourably inclined toward commodity prices as most recently written in the October 7th edition. Since then, long positions in corn and cotton have ‘timed out’ at the fifteen-day mark, leaving only a single long position in soybeans. As a reminder, all positions are subject to this ‘time-out’ and are only kept beyond that period if a favourable trend has developed – we only try to ‘run profits’ when there is a profit to run. There is an additional ten-day time-out that we impose in commodity markets due to their greater tendency to change state without warning on supply shocks. Corn and cotton had passed that hurdle but fell at the next – mostly due to a USDA report on Friday (one of those supply shifts).

There are conflicting influences beyond the usual ones in agricultural commodities right now. Population growth is astonishing and fast enough to make a difference even in a few years. The UN thinks that the world will hold 9.7 billion souls in 2050 compared with 7.3 billion today, passing 8.5 billion in 2030. That means 80 million more people – another Germany – each year. This obviously affects all commodity markets but food needs acreage that may get squeezed before long unless one of the other trends comes along to help. This population growth is all in Africa and poor Asia (i.e. not in China) but these folk will not stay poor for long. Fast movement of population from countryside to towns is normal when a bit of prosperity takes root and the resultant urban expansion increases the productivity of the people involved and so adds to global economic growth which keeps commodity demand growing briskly, with some setbacks as now.

Prosperity also leads to consumption changes as meat makes up more of the diet. Eating animals for food calories requires a lot more agricultural output than eating the crops themselves, as is widely acknowledged but this process is now continuous, due to the rural flight in these growing countries and the effects will be far larger than seen so far.

Climate change is the great bugbear of our era but some scientists have begun to mutter that it isn’t all bad – it is unwise to proclaim such heresy loudly unless you want to become a pariah but there are few more acute minds than Freeman Dyson, currently at the institute for advanced studies in Princeton. He notes that increased amounts of Carbon dioxide in the air (currently 400 parts per million, up from 300 ppm when this author was a boy) will stimulate plant growth and thereby limit that CO2 increase as plants use up more of it – this is negative feedback in action. This was intended as a rebuff to those who claim that we are in a runaway feedback loop that will lead to planetary doom but an obvious side-effect will be increased crop yields. Interestingly, the wheat yield record has been broken twice this year in two different parts of the world in an otherwise unremarkable year for sunshine or rain – it seems likely that the increased CO2 that surrounds us is already acting to boost production. This is not part of routine market commentary yet obviously should be a factor to consider as it is long-term in nature unlike the cyclical ‘El Nino’ phenomenon of surges in Pacific surface waters that comes (now for example) and goes.

So there are long-term bullish forces at work in all commodities – principally population growth but also urban expansion. There are long-term bearish forces that will increase crop yields (climate change) and others that will continue to have shorter-term negative effects such as weather and oceanic shifts like the presently building El Nino.

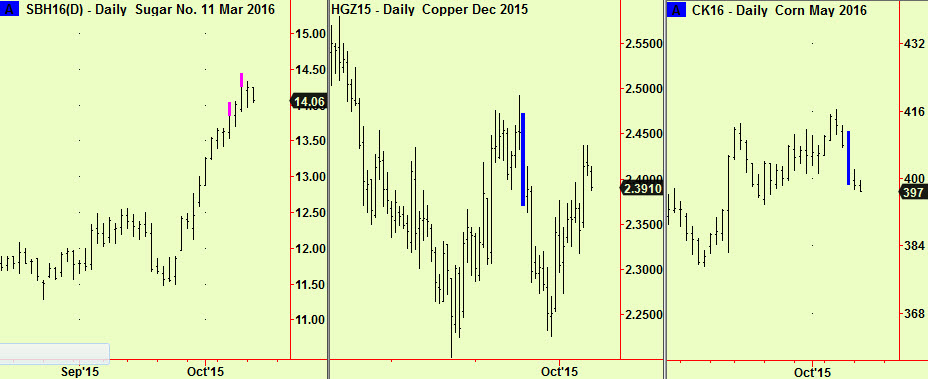

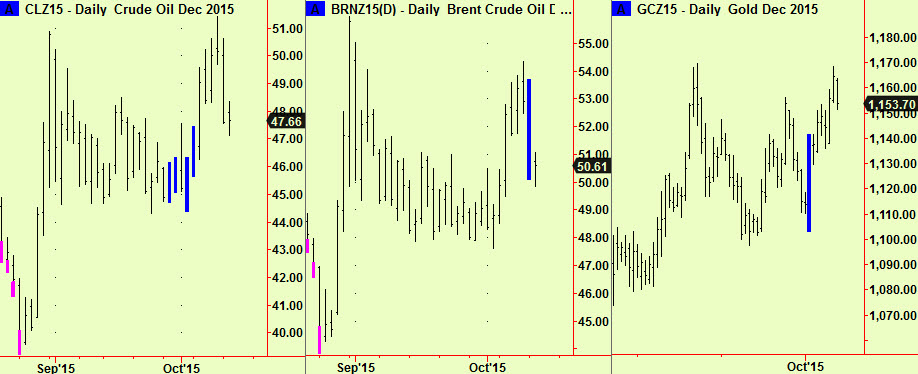

This means that commodities will remain a two-way street and that we will continue to recommend trades from both sides of the market. Currently we have five outstanding commodity trade suggestions that our portfolio has not had sufficient room to take – long positions in gold and crude oil and shorts in copper and (as of now) sugar and corn.

We are going to take two of the shorts. Copper has rallied deep into the compressed area that we pointed out recently and so can be sold short with close stops just above that compression. Sugar has just made top extensions at a daily scale and seems overdue a dip (at least). Corn has compressed and seems to have (just) broken downward as of yesterday but we will not take this corn trade (yet) because we will not have enough room:

The crude oil and gold trades look less compelling for different reasons. WTI crude compressed and moved up, falling back down to the level of those compressions in the last 24 hours. This would make a classic ‘buy the return to a compression’ trade except that Brent crude produced a new compression yesterday, which means that it is now a coin-flip as to which way the move develops. If that Brent compression breaks up in the next few days then a long trade will be doubly attractive. Gold compressed and broke up a few days ago but is now too far from the compression level to buy it without some concern about a dip. if there is a return to that compression, we may try to buy it – if we have room by then.

There is a large turn coming up in many markets on Thursday the 15th, this week. We may use this event to take profits on any outstanding trades, so it may be that some of these new (or recent) positions will not last their full 15-day life. We will advise.