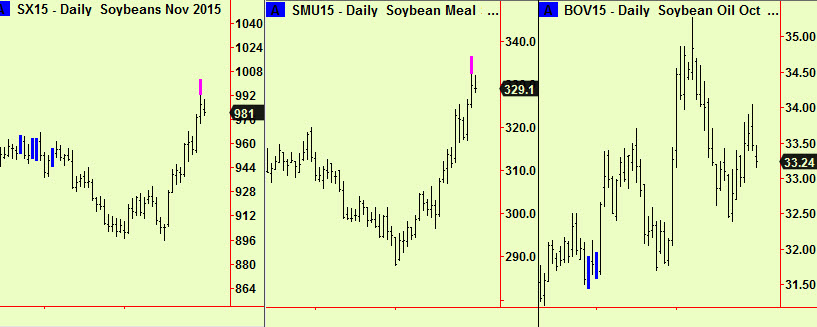

In yesterday’s session, soya beans and soya meal both made top extensions. We have been bullish about the grains in general and have already advised long positions in corn and soya beans, half of which remain after the usual part profit-take instructions. The remaining half long soya bean position may now be sold and we suggest trying a short position in soya oil here. There is no specific signal in soya oil but the logic remains the same as it has been for some years – demand for soya meal drives the market and soya oil is relegated to be something of a by-product. When sell signals appear (as now) we prefer to short-sell soya oil.

Elsewhere, stocks have been weak in response to the latest development in the Greece/Euro squabble. This has pushed US equity indices down to the lows of the recent trading range from which they are bouncing as I write. The rally in European indices stalled against resistance in the DAX, as pointed out in the June 23rd edition but we did not advise selling so cannot now re-buy as we would probably wish to do.

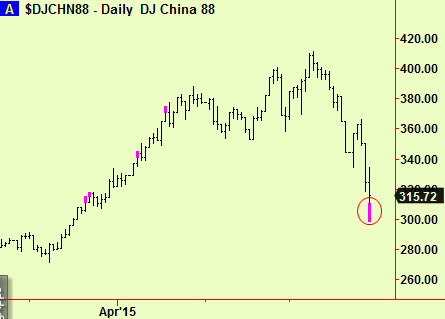

China made a bottom extension in the most recent session that finished a few hours ago. This market has been the weakest since we warned that ‘the picture has darkened somewhat for equities worldwide’ in the June 16th edition and it looks as though it may be time for a bounce there. This may coincide with rallies in other equity markets too as their trading ranges continue. Stay long of those stock markets we have recommended, with the same stop-losses in place and try buying some China. There are some equity turns due today, as our new display method at the bottom of this email shows, which seem to be coinciding with these lows.

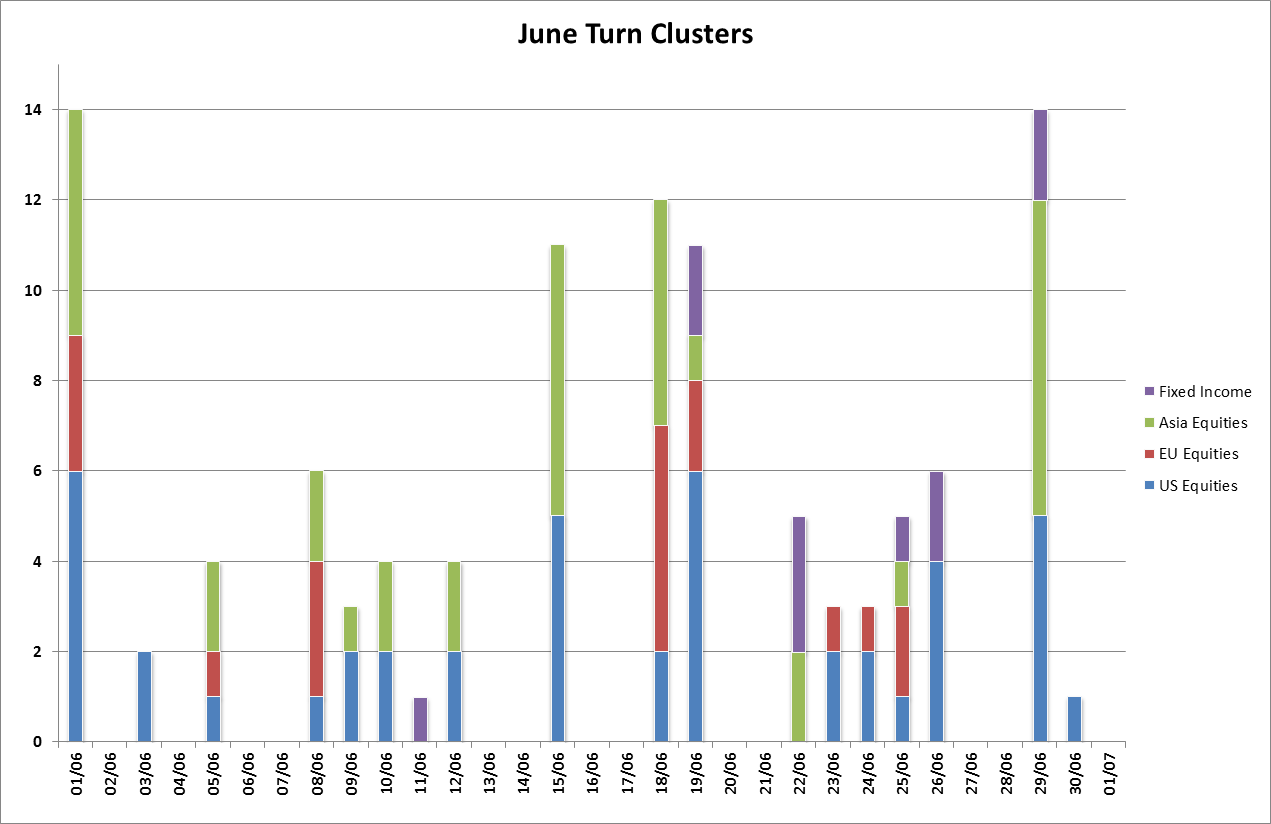

This next chart shows our new method for displaying turns. Instead of grading each turn cluster from 1-3 we now show the actual numbers of turns expected on each day, selected from the equity and bond categories shown. We will broaden this to include commodities and currencies in due course. July update coming soon.