Stock markets have diverged considerably around the world and there is no clarity at all about their next direction. Here is a survey of the situation in the main places of interest.

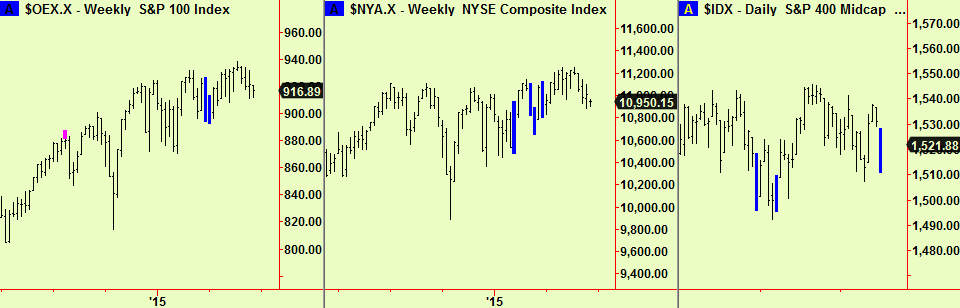

Several important US indices compressed at a weekly scale earlier in the year and briefly poked above the level of those compressions but there was no ‘follow-through ‘and prices are now back into the compressed areas again as the first two charts show. The last shows that fresh compressions are still occurring at a daily scale and so this range-bound condition has yet to resolve. It may be worth noting that a general background ‘bearishness’ has been apparent in the commentary sections of the financial press lately, in which various worthy market people have pronounced that prices are ‘too high’, referring mainly to US equity valuations. It is not impossible for prices to fall in the face of such bearish rumblings but it is unlikely – at least not yet. Until we see a break we are sidelined with half a long position split between two sector indices. Charts:

Europe has been a bit weak lately, distracted by the tragedy or farce of Greece. Greek membership of the Euro has had more farewells than Sylvie Guillem as it is taken as read that debt default must lead to expulsion. This doesn’t happen when a municipality defaults in the US but perhaps the taskmasters in Brussels are harder than those in Washington. It seems odd to drive a country that is at least notionally European into the welcoming arms of a resurgent Russia over a debt that everyone knows they cannot pay. The whole Euro project was driven by the politics of ‘ever-closer Europe’ as was the joining of Germany’s two currencies before that. It seems strange that the same negotiators that pushed those two mergers through should now threaten to expel a member of the club just because they finally noticed that a single currency harms some countries, just as it benefits others. Could it be that they are bluffing?

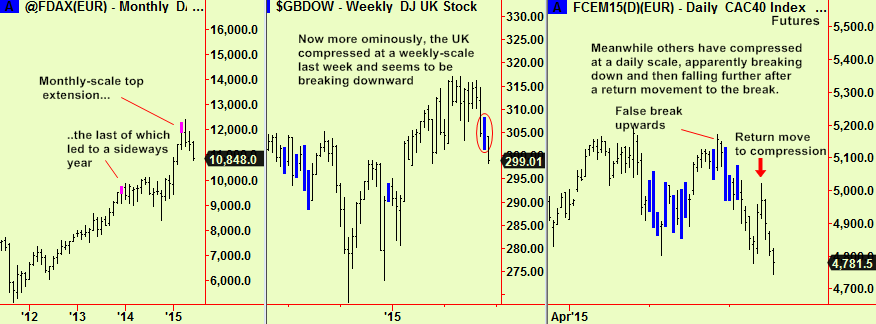

In the meantime, there were monthly-scale top extensions in several European equity indices earlier this year, the example shown below being Germany. This is not enough on its own to be an urgent bear signal as monthly signals are too imprecise, but now there is a new weekly-scale compression in one of the UK indices that we follow. This seems to be breaking down so far this week but we must wait until nearer the close of the week before we can act upon it. France has behaved in a similar manner to some of the others – here shown at a daily scale, where (after a false break upward that we unfortunately followed) it has re-compressed, broken down, returned to the compression and then fallen more. We did not take a short trade here, worried as we were that weekly-scale compressions were more important so missed the chance to make back losses from our failed long position. We wait.

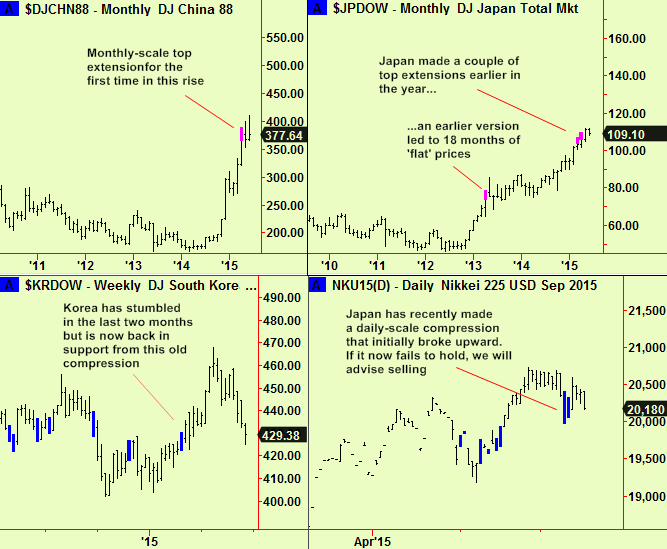

In Asia, the long-running China bull market has produced a monthly-scale top extension. As in the DAX example this is not enough to start a short-selling campaign but it is a warning that steepening uptrends are near to the ends of their lives, in time at least. The Japanese bull market is also producing the same signals whereas Korea (which never really joined in) has fallen back to support at an old weekly-scale compression.

The shorter-term Japanese position is more interesting as the recent pause led to a daily-scale compression that initially broke up but is now already being tested as support. If it holds then we may see another ‘upleg’ – there is very aggressive QE in Japan, so this would be no surprise. If it does not, then the whole edifice may start to crumble and we will start to look for short-sale chances.

The picture has darkened somewhat for equities worldwide but there remains a chance that ultra-easy money will push prices yet higher. We watch closely and will advise.