We started to warn of a potential large downward move in oil prices last year after we had noticed a feedback loop in the crude oil market that was likely to implode. Oil and related energy prices have fallen fast over the last few months so this is a good moment to review the causes.

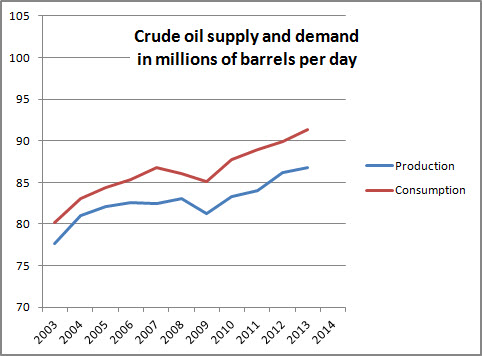

Supplies were said to be ‘tight’ as recently as last spring and the demand vs supply picture for crude oil still looked to continue in a similar trend over years – this is the chart of each through end-2013:

These two well-established trends are both upward but consumption is growing faster than production by about 200,000 barrels per day. Seeing this led many to predict an imminent crisis in world energy supplies, including some hysteria about ‘peak oil’ some years ago (which illustrates the danger of extrapolating trend lines). The data is real but makes no allowance for changes in the world and the nature of production.

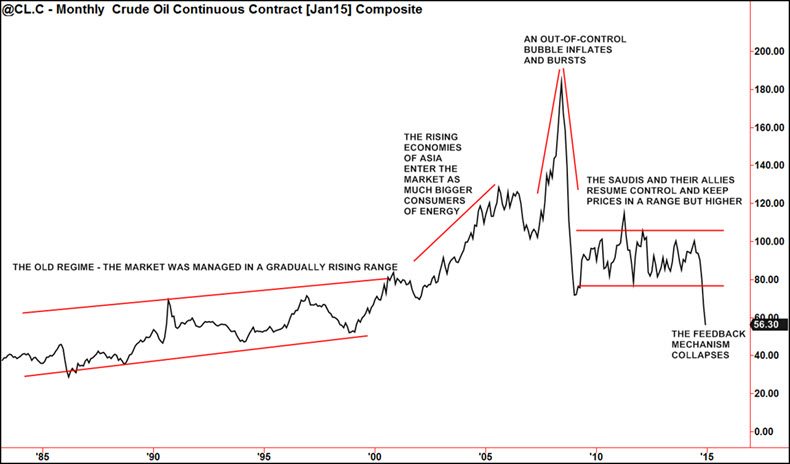

Obviously these numbers don’t tell the whole story, no matter how convincing they look, as they make an ever-rising price seem inevitable. A bit of history may help. Oil prices were kept artificially low in the post-colonial era until the oil producing countries of Opec realised that power really had drained away from Britain and France, their old masters and so they engineered an overnight tripling of price in 1973. This ‘oil price shock’ as it was described at the time was a nasty surprise and a recession quickly followed in the industrial economies. Another rise occurred in 1979 when the Khomeini revolution toppled the Shah of Persia to install the present Islamic Paradise of Iran. Prices remained high and much oil was traded on fixed-term fixed price deals instead of the auction market that prevails today.

By this time Saudi Arabia was the pre-eminent force in the Opec cartel by virtue of its huge reserves and large pumping capacity. The urbane and clever Saudi Oil minister of the time took the sensible view that his main customers were in the West, which was also the home of innovation and technology. If oil prices were pushed too high this would soon mean that alternative sources of energy would be exploited, such as the enormous Athabasca Tar Sands of North-Eastern Alberta or various sorts of nuclear power. The Saudi powers-that-were took the decision to make sure that prices didn’t rise too much, so as to guarantee themselves continued revenues in the long-term. Prices were already high enough by the late 1970s/early 1980s to explore underwater and produce from Alaska and the North Sea but volumes were always likely to be too low to be a threat compared with Saudi Arabia’s potential to produce up to 12m barrels a day at almost no cost. The main potential rival sources would only start to look viable if oil prices were much higher – say $80 a barrel or more.

Throughout this period and into the 2000s Saudi Arabia, mostly with its Arabian Gulf allies, successfully maintained its role as the ‘swing producer’, cutting production when prices dipped and raising output when prices rose, so achieving reasonable stability.

Many of the other Opec members occasionally shouted that ever higher prices were only right and just but they were merely passengers in the boat and the Saudis kept to their plan to ensure that prices stayed high but not too high. Managing this situation cannot ever be a precisely calculated activity among so many competing buyers and sellers but their dogged presence as a generous seller on rallies and a reduced seller when prices dipped created a feedback loop that kept prices in a cyclical range between $45 and $60 for most of the 1990s. This is the normal consequence of a major player ‘leaning against’ market moves and explains why there is a business cycle in the US as the Fed does the same with interest rates in normal times – see our videos for more on feedback driven cycles.

This was sometimes costly for Saudi Arabia and their treasury experienced a cash squeeze in the early 2000s that led to the embarrassment of needing a secret loan from the UAE. This was chastening for the Saudis who had started spending much too freely on questionable projects and may have led to what happened next.

When China and the other emerging countries of the Orient added their growing energy demand to the fairly balanced situation that already existed, prices naturally rose. This reached a climax in July 2008 when the prices of WTI crude rose close to $200 before dropping in a straight line to a low of $64 seven months later. By this time, innovation in the US oil and gas industry had just (in 1998) made extraction from so-called ‘tight oil’ from shale deposits technically possible by fracking and the high and rising prices of the period 2000-2008 had made this novel form of extraction profitable too.

Prices soon recovered from that early 2009 low and the Saudis resumed control of the market, this time deciding that higher prices were now appropriate and so we saw a highly cyclical trading range develop for the next five years until October this year, between about $80 and $100 with occasional brief moves outside the range. This seemed to be a triumph of market command and control but the Saudis had made a mistake in choosing too high a price. Many more sources of oil are viable above $80 than in the old range of $45 to $60 and this potential supply had expanded greatly because of various oil industry innovations, including fracking. The policy of ‘high prices but not too high’ had worked to keep the Saudis rich and the industrial nations dependent on their oil but they had fatally wounded the golden goose.

Now that oil and gas can be produced in steady streams at medium cost ($50 a barrel and falling) the Saudi response has been to follow one blunder with another. Having allowed prices to stay too high for too long and so encourage the new supplies which are increasingly making the US energy-independent, they have now abandoned the feedback mechanism that they created. By continuing to pump as prices fall, the drop is made worse and this is explained by some commentators as ‘protecting market share’. It is worth examining what this means. In a market for manufactured items, such as cars or cameras success depends on many attributes of quality, service and delivery and so market share may be built up and defended by improving any or all of these. Oil is a largely generic product and so users are far more interested in price than in say, aftermarket customer care.

That means the principle way to defend market share will be by putting rivals out of business and that seems to be the likely motive for the Gulf countries to sell into a falling market, as they are now doing. The aim appears to be to harm the existing fracking activity in the US and to deter any moves to establish it in Europe and elsewhere. For the Gulf Arab states there is the pleasing secondary effect of watching their arch enemies in Iran suffer further economic damage from these low oil prices on top of that already done by US sanctions.

What happens next? This current manoeuvre will probably fail in its intended objective as the economics of the new kinds of extraction are different from those of the oil industry in the past. Then it was necessary to risk large amounts on exploration – expecting to drill lots of ‘dry holes’ – and further deploy huge amounts of capital on deep sea extraction, tankers or lengthy pipelines. This is not true of the new methods, as the location of many substantial ‘tight’ energy deposits is well known and they are easily accessible inside the borders of the US – and in Europe, if good sense is allowed to triumph over shrill protests from the ecologically illiterate. Capital costs are also modest compared to the energy yielded and this is spread over many wells, which have to be drilled often and then managed by pumping in water, sand and some chemicals. This makes each well cheap to drill but relatively expensive to run, meaning that this activity will be more responsive to price moves than in the former days of major heroic high-cost oil projects which kept pumping through all conditions, as the major costs had already been incurred.

As a result, this new form of oil and gas extraction is almost impossible to kill off with suicidal pricing. Some fracking developers will go bust, if prices remain low and some loans will default but the technology cannot be uninvented and will always be available to deploy, when prices are high enough, in the tight oil and gas fields that are already identified. This current clumsy and spiteful attempt to put a rival producing industry out of business will surely fail but it may take some time for this to become apparent. How long Saudi Arabia and the other Gulf Arab states can keep this up will depend on how quickly they realise this, with the attendant loss of face when they acknowledge that they have failed but it will also depend particularly on how long Saudi Arabia’s financial reserves can last:

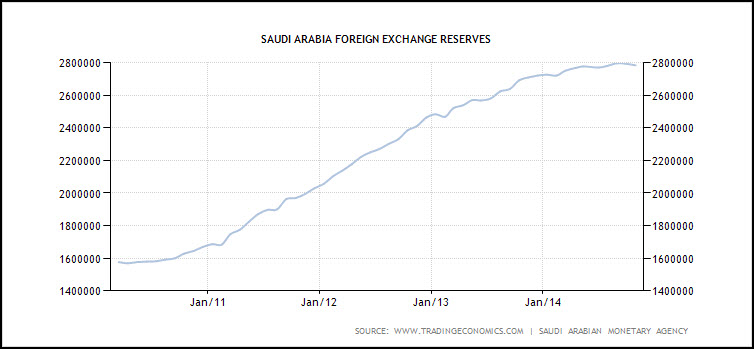

On the face of it the financial situation looks robust. The reserves are shown here in Saudi Riyals and they have doubled over the last four years to the equivalent of $750bn.

This is not as good as it looks because doubling in such a short time shows that this is volatile and so can decrease just as fast or even faster. This apparently high number also represents only 36 months of imports. When reserves were half as big four years ago, they equated to 30 months of imports so we can deduce that this substantial expansion in financial resources has been outweighed by a huge increase in Saudi spending abroad in that four years. This spending on trinkets, welfare and aid to local allies is essential to preserve the status quo in the region and in Saudi society, from where there are already more and more recruits joining jihadi groups. It is inconceivable that the Saudi authorities will embark on any form of austerity for fear of their very lives – the country is run as a family business that pays protection money to its population who are less and less satisfied with the arrangement. Arab regimes rarely end peacefully, so the few thousand princelings that most benefit from this massive oligarchy are nervously aware of the consequences of failure. Spending will continue at least at current levels, so expect the financial strains to show up sooner rather than later. In the meantime oil prices are likely to remain under pressure.

For prior articles on this see our archive: