Now that the Petulant Pygmy’s war looks less like a blitzkrieg and more like a traditional meat grinder, markets are adjusting to the prospect of a long conflict with the ever-present danger of it widening, even to the extent of nuclear weapon use. We laid out our four main themes on February 24th just prior to the awful beginning with some updates a few days later. Here is a longer look at those themes. They were:

Short US stocks (originally January 24th 2022, most recently February 11th 2022)

Long Gold (originally June 21st 2021, most recently February 11th 2022)

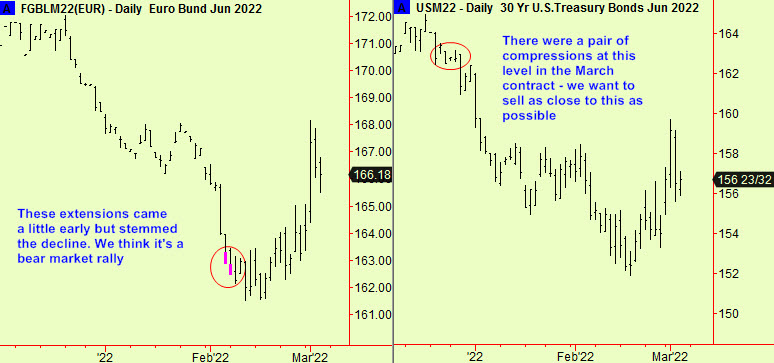

A bounce in bonds that we want to sell (many editions, including the bad pun on January 12th, & recently February 11th

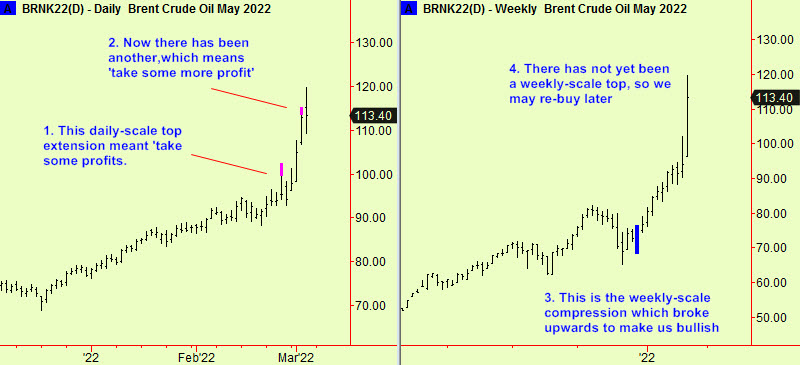

Bullish energy (since January 12th)

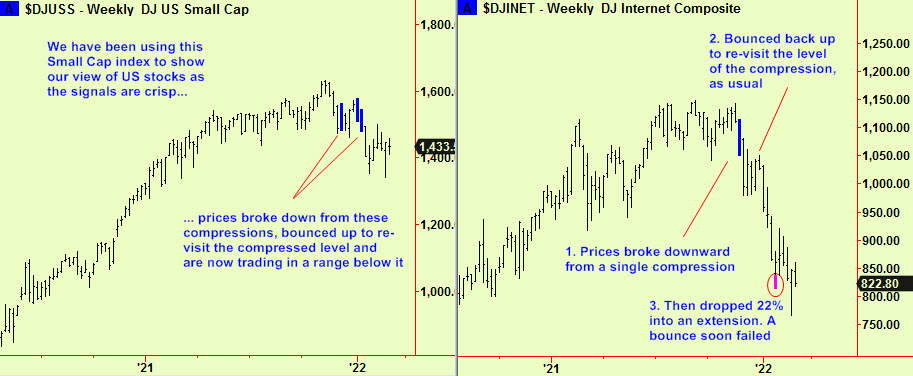

Short US stocks. This view was noting to do with the prospect of war and all to do with the break down from some weekly-scale compressions, as reported here many times. We expected a bounce in all stock markets after the drops of the 24th February and even advised buying some European indices for that bounce, expected in the subsequent days. This did not affect our longer-term view and we expect the bounce to fail. The timing of this may depend on events (where we have no ‘edge’) but if it is a function of the crowd dynamic (where we do have that edge) then it will either happen because of an imminent turn cluster or some extension/compression signal that we haven’t seen yet. This month is particularly ‘turn rich’ as the Schedule on our front page shows. The first of the cluster of these expected turns comes on next Tuesday 8th March and there are several others in the days to follow. Closely-spaced large turns like this often mean wild gyrations, so be very careful! Here are updates to two of the charts we have been using to illustrate our views:

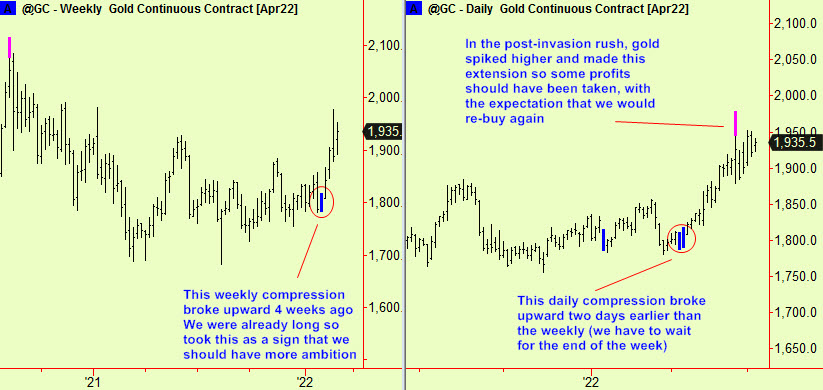

Long Gold. This position is based on both daily- and weekly-scale signals. Here are updates, weekly first. As it says in the daily chart legend, we would have taken/would take some profit, looking to re-buy later:

A bounce in bonds. Bonds did indeed bounce and we do still want to sell them. We didn’t find a reason to do that yet and it is quite possible that we will miss the best chance to do so. We posted levels in the January 24th edition which are updated in the bond chart below – it didn’t get quite that high on Monday’s rally. We watch carefully – here’s an update:

Bullish energy. This view comes from weekly-scale signals, which are updated in the second chart below. There were some daily-scale top extensions in various energy futures on the invasion that we reported in the February 25th edition which would have meant taking partial profits (same as in Gold) but prices quickly continued upward. Now there has been another daily-scale top extension, so we would take more (all?) profits and wait:

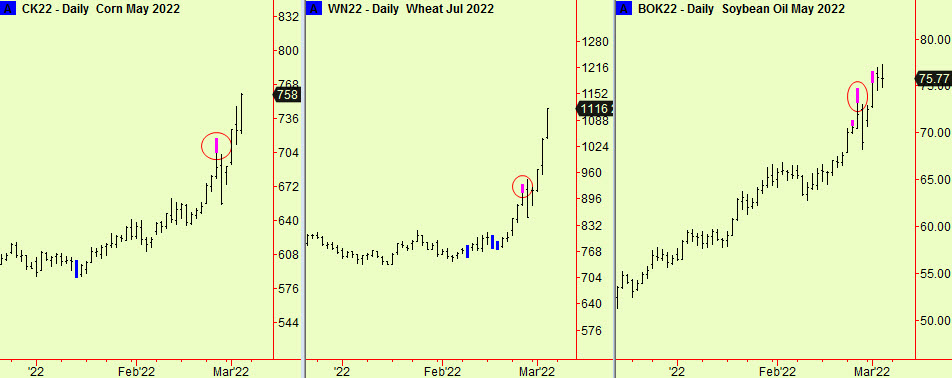

Lastly, grains. We reported top extensions in Corn, Wheat and Soya Oil in the February 25th edition. These led to a one-day dip that had already occurred by the time we reported these signals. Events then took over and the prospect of a longer, wider conflict that would harm grain production and/or exports pushed prices even higher, especially for wheat. Ukraine produces almost as much wheat as Canada, so this would dent world production by as much as 4%. We almost never advise selling short merely because of a top extension, and neither do we here. An update:

All signals generated by software produced by our friends at Parallax Financial Research www.pfr.com