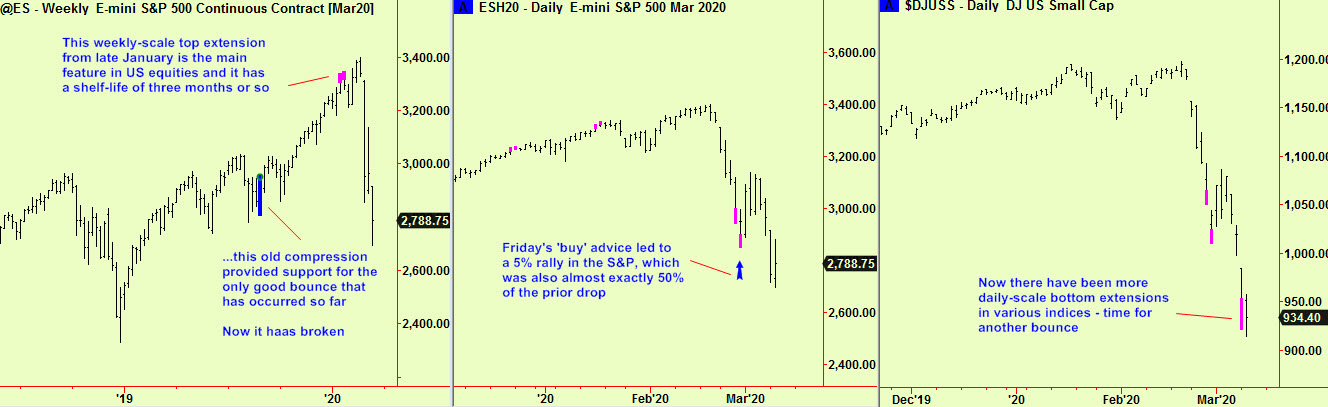

The drop in stocks since the brief rally high on Tuesday the 3rd has taken many indices to new lows for the move. The weekly-scale top extensions that occurred in late January will remain the dominant feature of our analysis for several more weeks, but in the mean time we will try to ‘call the turns’ as best we can. The ‘cover and buy’ recommendation on Friday 28th led to a brisk 2-day 5% rally before renewed weakness set in late in the week and into early this week. Now we have yet more daily-scale bottom extensions and so we expect the drop to end or pause again, hereabouts.

Sharp 1-3 day rallies are typical behaviour for bear markets and should be regarded as chances to re-sell – see the 18th/19th September 2008 for a particularly vivid US example. We do not expect a full-blown bear market to develop (yet, if at all) and still think that a trading range is the more likely outcome. As we wrote in the March 2 edition, such ranges can be ‘wild and wide’ as events have confirmed. Don’t press on the short side here and don’t be shy about trying to buy. Keep it tight though and don’t risk much as volatility will remain high.

Energy markets have collapsed (except for Natural Gas which has rebounded sharply) and we missed this completely. The contest between the one-man show that is Russia with the other one-man show that is Saudi Arabia seems to be a bigger replay of the situation in 2014 when the Saudis first cranked up production as an economic weapon. This action, taken under the present crown prince’s predecessor was intended to harm Saudi Arabia’s several oil-producing opponents and to inhibit fracking in the US. Fracking had been encouraged (or even created) by an earlier Saudi mistake in 2008 when they allowed prices to climb far above the previous ‘consensual’ range and so encouraged all kinds of ‘tight oil’ exploitation – something they had been scrupulous in avoiding when they were better-advised through the prior decades. Now, the genie is out of the bottle and fracking exists. The location of many promising fields is well-known, the technology is cheap and the capital required is modest, both to drill and to extract. Low prices will not make Fracking disappear – it will only suppress it. Nothing has been learned, it seems.

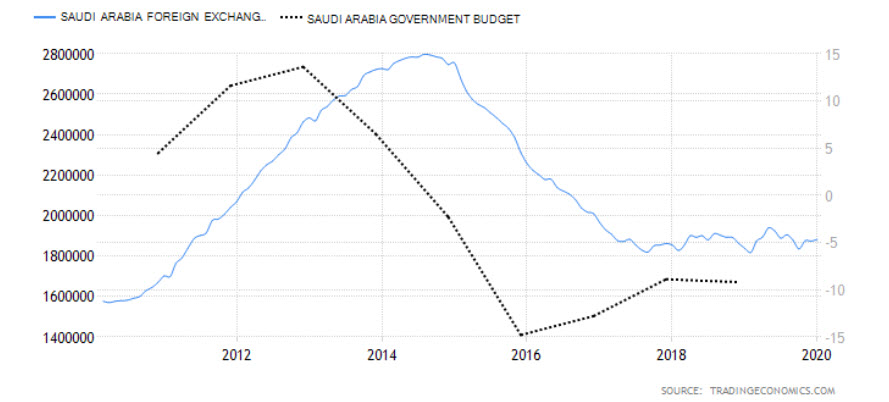

In the meantime, Saudi Arabia is said to need a price of $80 per barrel to balance its budget, which relies on heavy social spending to maintain the Al-Saud family in charge and heavy military spending to keep its status as a big player in the region. This chart shows their perilous financial position, plotting reserves against changes in government spending, which started to drop from 2015 when reserves were still comfortably high. This position will only get worse with oil at multi-year lows unless the kingdom resorts to borrowing (‘Haram’ in Islam, if interest is involved). The country is inherently unstable and this foolish move to push prices down could be the push that takes it over the edge into regime change. That would be far worse than anything we have seen in Iraq or Libya and would result in oil prices at record highs:

We regard this as a good chance to add to Natural Gas longs, as prices have dropped in temporary sympathy with crude oil and the other energy markets and then quickly rebounded- there is a different dynamic operating in Nat Gas and it should take prices higher soon.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com