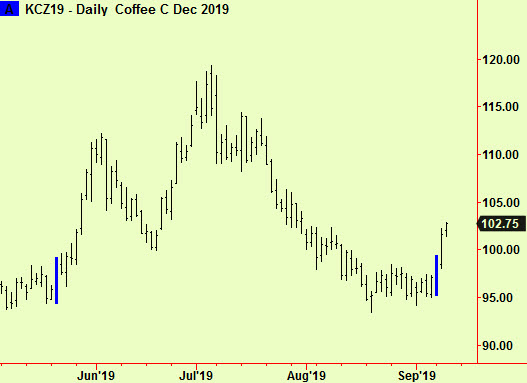

There was a daily-scale compression in NY coffee futures two days ago that broke upward yesterday:

As you can see from the earlier compression in this same chart, such breaks can start a run-up that can go for some distance before any reaction starts. There is usually a return back to the compression (as there was in that earlier example) before the move resumes but it can be an anxious wait. Buy any tiny dip. This fits with our general bullish posture in commodities, where we expect to continue providing ‘buy’ signals one-by-one.

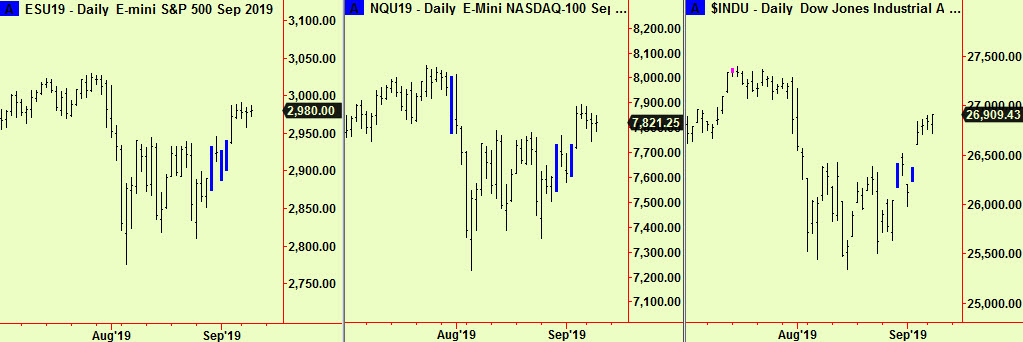

The picture in stocks has clouded again – this is normal in a range, which is what we think is still the main feature, as it has been for two years in the US and even longer in international markets. The main US indices all broke upward from compressions, as we first pointed out in the August 30 edition:

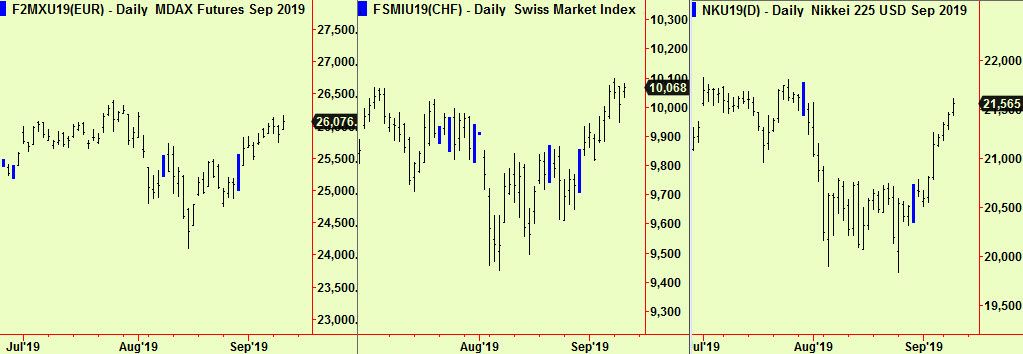

They have all made some gains since that break but progress in the Nasdaq has been slight and all have formed tight ranges in the last few days. Other indices around the world have performed much the same and here is an update on the two Europeans and the Nikkei that we first showed in that same edition:

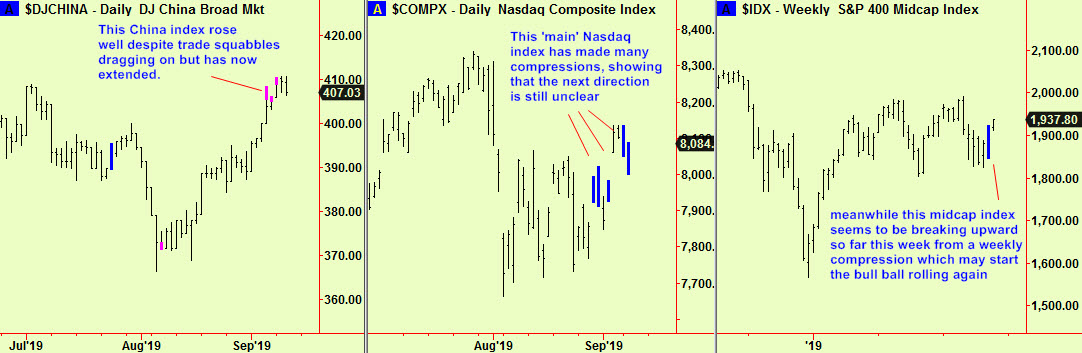

We have recommended holding on to longs that we advised taking in the August 16th edition and that advice remains the same. We are seeing some reasons to think that there may be some more ‘churning’ however and so we would tighten stops or maybe take partial profits.

The main reason for caution is a series of daily top extensions in China but there have also been more daily-scale compressions in some US indices, including the broader Nasdaq (not all indices have gone up, some have traded sideways) and another weekly version in the main midcap index, the S&P400. This last one seems to be breaking up so far this week, but the week isn’t over yet:

There is of course no reason why a top extension in China should inhibit the behaviour of US markets, as the main connection between the two is their similar responses to the US president’s tweeted sudden policy shifts.

The Chinese economy is much more vulnerable to a downturn in trade between the two countries as US goods and services exported to China are just less than 1% of the US economy while the reverse flow accounts for over 4% of China’s*. It is entirely possible that US equities could rise while shares in Chinese companies might fall. We have written in the June 14th edition that the US/China trade dispute is likely to simmer on in a state of stalemate because of fundamental differences that cannot be negotiated away, but there will be occasional bright spots in the general gloom.

*According to the Office of the US Trade Representative

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com