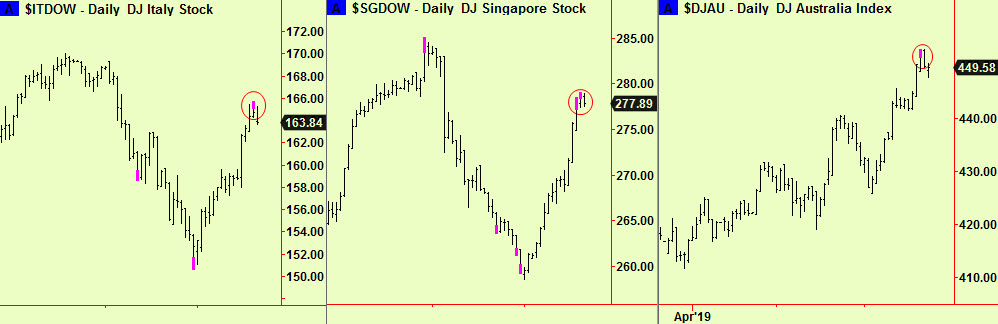

There has been a further scattering of top extensions in equity markets, all at a daily scale:

US equity markets have also risen but there have not yet been any top extensions. We still take the view that profits should be taken on any long positions in all the broader equity indices and that you should start to adopt a bearish view. As ever when top extensions happen, it is wise to wait for some signs that the rally is over and that some kind of top has formed before selling aggressively short. We would make a start however, as argued below.

Not all equity markets have risen. There has been a period of sideways trading in some, for example Norway, Spain and Japan. All these national indices have compressed, the first two at a weekly scale, so it is reasonable to suppose that some increased volatility is imminent, probably a new trend:

It is hard to see how these three can break upward from these compressions into new uptrends in the face of the top extensions reported here and in Switzerland in the last edition) so we are tempted to say that they will weaken instead. We can never tell which way compressions will break, so this is not a forecast, merely a clue to be considered together with the top extensions shown higher up the page.

Elsewhere, the Fed’s apparent shift toward a looser policy and the ECB’s apparent willingness to apply fresh stimulus in the Eurozone has boosted other assets too. We reported that Bunds had made a top extension in that last edition and that the other European bond markets (and US treasuries) could be sold short. We still hold that view, but this is tactical advice only – as we have pointed out several times in recent months, selling bonds short while QE is still a weapon in the armory of central banks is dangerous. There were hundreds of trading casualties among those who tried to do this in the years after Japan was the first country to deploy QE (in 2001) and Japanese bonds rose and rose and never ever fell back to pre-QE levels. That may not happen in the US but it seems likely that it will in Europe as the economy remains stuck with a pointless unified currency that inhibits the growth of the southern countries while stimulating Germany, without any proper mechanism to redistribute this disproportionate windfall for the Germans. This will keep monetary policy ultra-loose for a generation or until Germany realises that they are not the winners by virtue of their superior attributes compared with the feckless members of the garlic belt but are instead the beneficiaries of a rigged game. Southern European pain is the direct converse consequence but this argument isn’t understood in Germany and there seems to be no chance of a change of heart.

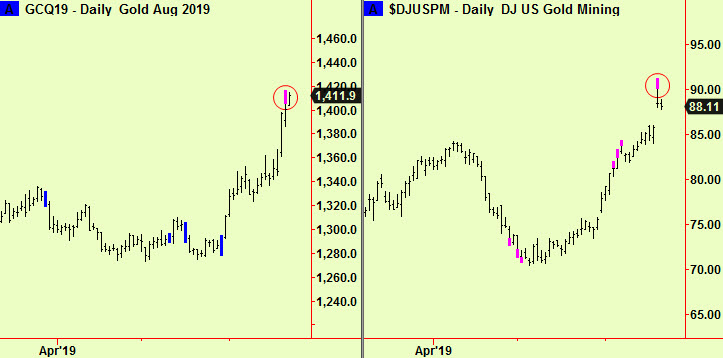

The general rally in assets has included Gold, which has now also extended, as have gold mining stocks:

This is a little odd as the world is probably deflating more than it is inflating and gold’s strength probably has more to do with the recent weakness of the $ than any flight into the pre-eminent ‘shelter asset’. If you own some, sell it but don’t sell short yet for the usual reasons we give when reporting top extensions (see above).

On the subject of the US$, we have no signals to indicate whether this current weakness is the start of something bigger or if it is just a wiggle within the range. We have been searching all currency pairs for clues but there is nothing to report. When there is, we will

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com