The recent sharp rally in US Treasuries has resulted in a daily-scale top extension. This is typical of the saw-tooth pattern that seems to be developing, in which a very gradual uptrend underpins a jagged series of highs. It is dangerous to become bearish of any government bond market while QE is still an accepted tool for central banks to use for demand management but that doesn’t mean that prices won’t occasionally fall. That looks likely from hereabouts:

There have been no such signals in any European government bond, despite the fall in ten-year German Bund yields to the same low (-0.16%) reached in 2016. The entire German government yield curve out through ten years is now negative, meaning that fear is still the main motivating force here and Germany is the most creditworthy debtor in the Eurozone. It is always worth remembering what happened in Japan in the 1990s when their central bank became the first to deploy what is now called Quantitative Easing. Interest rates went lower and lower and bond yields too. Anyone who sold Japanese government bonds short for more than a few weeks lost money. That was in the face of a prolonged decline in Japanese economic growth (which has not happened in Germany, but has in the wider Eurozone) and the same situation still exists in Japan today, almost 30 years on. We continue to look for place to adopt ‘tactical’ short sales in all bond markets but this historic parallel between Japan then and Eurozone Europe now is dangerous to ignore.

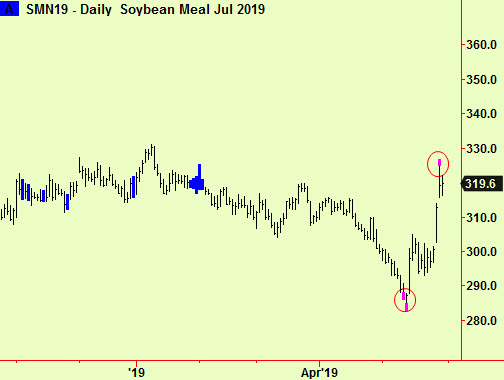

Elsewhere, the sharp rally in grains has obviously dented the prevailing bear market (as we warned repeatedly, most recently in the May 8th edition) and even soya products have now joined in, despite lagging for the first ten days. There have been top extensions at a daily scale in corn, as we reported last week and now in soya meal too:

These signals do not tempt us to become bearish as this rally seems to be the start of that new market phase we had anticipated. The speed of the ascent has been quick however, and it has all the signs of a short squeeze, so we would book (or at least protect) some profits here as price volatility is likely to continue in the short-term. If you trade out of any long positions, replace them on dips, as we already recommended on May 21st.

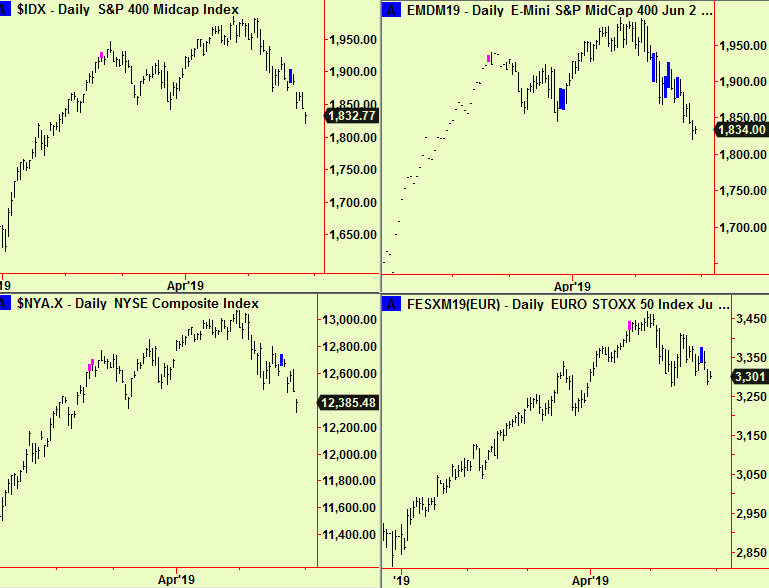

US Stocks (and the Eurostoxx) have pushed down through the compression signals that we reported in the May 22 edition, and here is an update of the same 4 charts we published then:

If you ‘sold the break’ then stay short. If you did not, wait to see if there is a bounce back up to the level of those compression, as usually happens before the price move continues before short-selling then. Protective stops should be placed above these compressions. We will watch for more clues and report..

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com