US and European Stocks continue to range-trade. As we have written, this may continue for some considerable time to come and price movement will typically consist of:

- Moves, both upward and downward that may be sharp. These are mini-trends that may last for some days or a few weeks

- Erratic behaviour within these mini trends that will produce some wide-ranging days – commentators will write about ‘the return of volatility’ but it will be short-lived

- Compressions will continue to appear, at both weekly and daily scales. Price ranges will tend to increase after these signals but it won’t lead to anything more than another mini-trend

- The range may itself become erratic and loosely-defined. There may not be clear boundaries at the high and low ends but any ‘range extension’ in which prices shoot through a previous high or low will be a trap for the unwary

This must be set against some risk that these ranges will break earlier than we anticipate – see the US section below

In these circumstances, successful trading will require nimble responses and a willingness to take profits instead of hanging on in the hope of greater gain. We advised buying Japanese and Swiss stocks in the July 5th edition which both have decent profits – don’t let them escape, even though prices are not yet obviously at the high end of the ranges.

Not all markets will conform exactly to this template – some will have trends, but these will be more like ‘sloping ranges’ or ‘shallow channels’. For example, France seems to have the potential to make new highs, as shown in the last chart below, but this will probably not lead to a steeper rise.

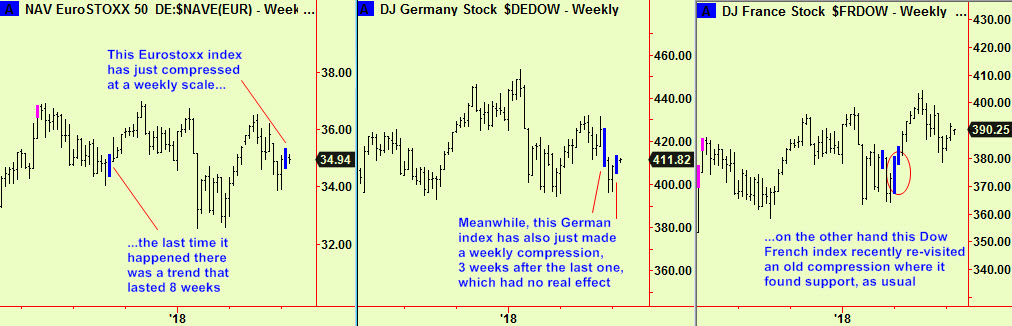

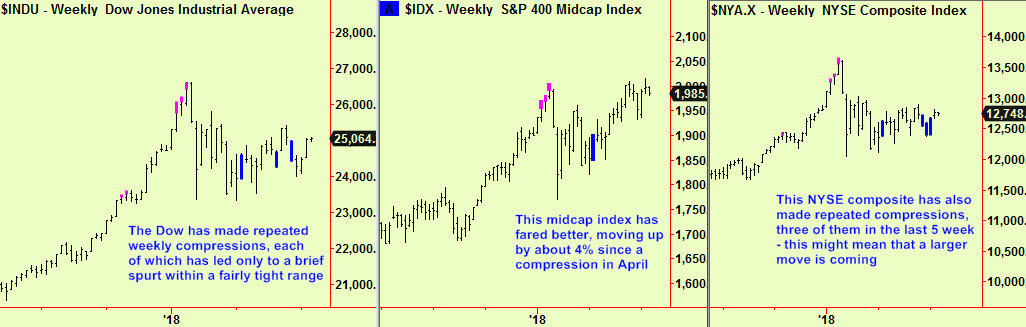

Europe

There have been some more compression signals, both in the main Eurostoxx index and a Dow version of the German equity index (and others, not shown):

US

The situation in US markets is similar, where compressions have recurred within the range. There have been a lot more recently in some indices – see the NYSE composite in the last chart as an example – which could be a warning that the range is not as safe as we think:

We will comment further on this as more evidence comes in – for now, keep range-trading.

Asia – China

We took a more bearish view of the prospects for Chinese Asia when a weekly-scale compression formed in a Hong Kong index and broke lower – this is how bear markets start, we said in the June 20th edition. Next, we reported a daily-scale bottom extension that ended that bear view (for now) in the 28th June edition. There have since been weekly-scale bottom extensions. so it seems that the China market will continue to hold and may rally for a while longer – these signals typically have a shelf life of three or four months. Bottom extensions are our single most reliable signal, so a stronger bounce is possible from hereabouts but the market will have great difficulty pushing up through the levels of that Hong Kong compression, which starts about 4% above current levels. On balance, we think that China is in the grip of a bear market and so it is premature to buy for anything other than temporary trading chances – the danger lies to the downside.

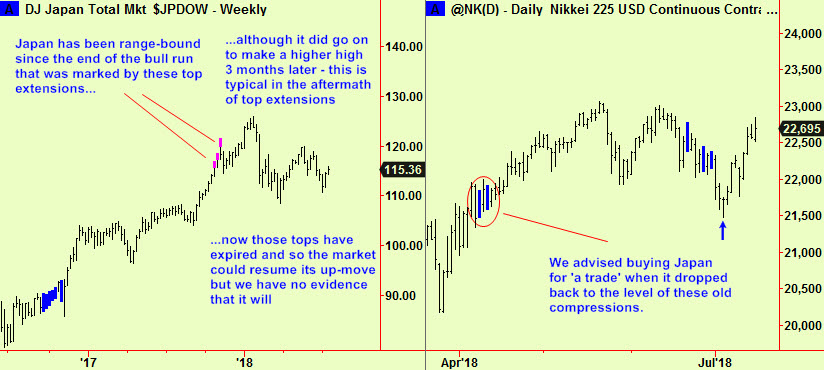

Asia – Japan

Japan has range-traded for even longer than the US. The bull market ended in November and an erratic range started then and continues today. There are no current weekly or monthly signals that would provide any medium or long-term clues so we remain tactically inclined. Out last advice was to buy it when in support (see second chart, below) as a safer alternative than buying China and that trade now has 1000 Nikkei points profit. It seems sensible to take it (as we always advise in a trading range) and wait.

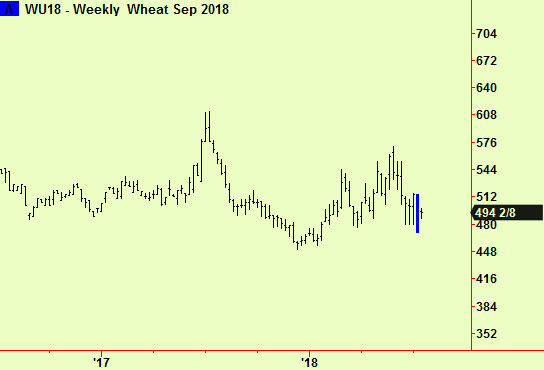

Elsewhere, there has been a weekly-scale compression in Wheat. We have been bullishly inclined toward Corn and Soybeans since seeing some bottom extensions in those futures markets last month but this is the first signal in wheat. We write from time to time about the parallel growth in demand (more and more mouths to feed) and the growth in crop size (more CO2) and it is worth remarking again that the growth in demand is ‘solid’ yet the growth in supply is still dependent on the vagaries of the weather. The crops are in fair shape (we read) so leaving little room for a shortfall at any near time in the future and the market has focussed on the trade wars that we think are actually not going to happen. We will write on that point soon. That has pushed prices down across the board and yet the net world supply vs demand equation is unaltered by this. Some soybeans may go from Brazil to China instead of from Illinois but the world will consume the same amount.

We suspect that there will be a sharp rebound in grain prices soon and we watch for clues as to when we should ‘jump in’. The chart:

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com