We pointed out the likelihood of more weakness in corn and the soya complex in our last edition, on June 6th. Both have fallen and now there is a bottom extension in soya meal that means the drop will probably end hereabouts. This new signal may lead to more than a bounce as the weekly scale top extension that led to the recent trading range is now almost expired and so the market could eventually push to new highs. There will be some resistance at the level of the recent daily-scale compressions (about $20 above current levels) that may hold prices for a while, so we have modest expectations, for now.

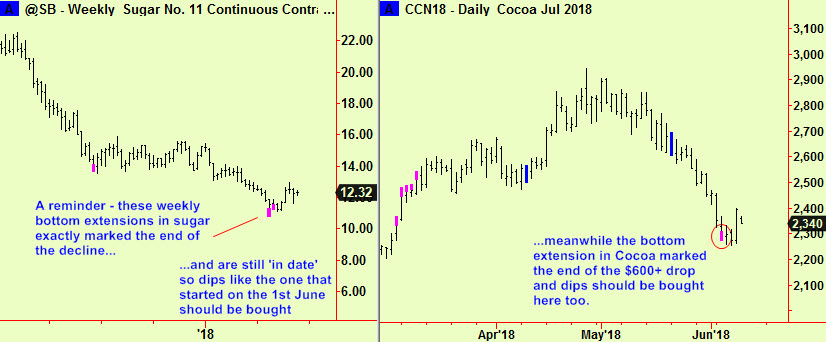

Elsewhere, the sugar market has recently been active, starting a price dip on June 1st that probably ended last week, on Friday the 8th followed by a sharp rally. The weekly bottom extensions at the end of April that stemmed the long decline from the end of 2016, in which prices halved, are still well within their expected shelf life and so dips in sugar can and should be bought. The price may not resume the higher levels of 2016 but bear markets in commodities tend to end with some ‘bumping along the bottom’ and that is probably what we are seeing here.

Cocoa also made a bottom extension, as we reported in the last edition and that seems to have marked the end of the recent drop. Buy dips

All this gathering evidence points in the same direction – the end of weakness in various (probably not all) crop commodities and the start of a rally phase. Be careful as the shelf-life of a daily-scale signal is only about three weeks, so any rallies based on that time-frame may be brief. On the other hand we have seen plenty of previous examples of medium and long-term market moves that have started with daily-scale signals but continued with more evidence developing later. This could be the start of something bigger and we will comment as events unfold.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com