The various calls we have made lately in stocks, bonds and currencies have been quite short-term because:

- By their nature we always get more short-term signals, so we make a lot more short-term calls

- There are outstanding weekly and monthly compression signals that have yet to resolve, meaning that many markets are still range-bound.

Examples, from US equities, where weekly compressions have yet to break:

The last chart simply points out that not every equity measure is range-bound and that there has been some enthusiasm for small cap stocks in the post-Trump-tax-cut period. We leave it to others to interpret what this particular ‘rotation’ might mean but to us it marks another warning that the main bull market is probably over and that we are looking at ranges that will continue in the main market indices until a new trend is warranted – probably downward, but we will be guided by the signals.

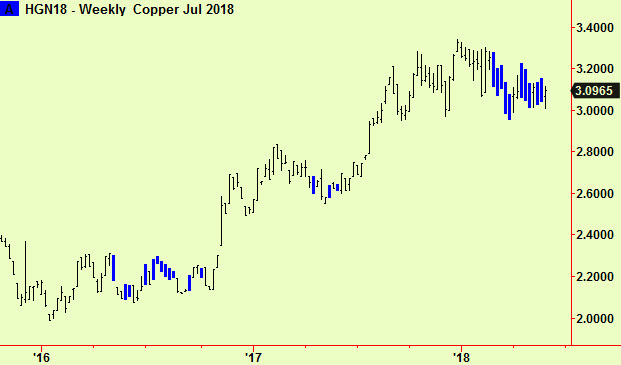

Copper is a bellwether for the economy, we always hear although there is less truth to that observation in this post-industrial era. It too has been stuck in a fairly tight trading range for a long time, making compressions as it goes. We still have a slight bias to the downside, for reasons given in the May 11th edition and one of those from April 19th but again we will follow the signals. Here is an update, just to point out that the range continues and so do the compressions. No break yet:

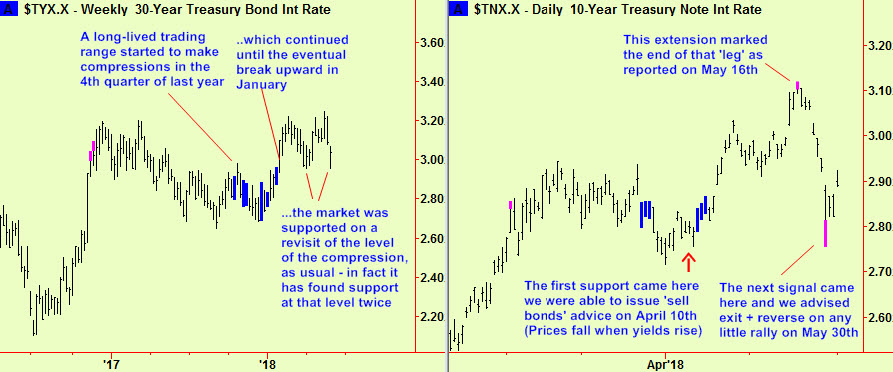

Bonds are different. There, a prolonged trading range led to weekly-scale compressions that eventually broke and the market has been quite easy to read through our spectacles since then – this after a long period in which we have not had any ‘edge’ at all as the market has been managed by the Treasury, not by free trading. Bonds are now ‘on the move’ and we expect more signals at all time frames as the larger moves unfold – you should now be short, as recommended (on any rally) in the May 30th edition. There was a suitable rally the next day. A summary, using yield charts, which are the inverse of the price:

More on other assets, including grains, soon.

RE

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com