As stocks rally from the bottom extensions that showed up in a few scattered European indices earlier in the month (see November 16th edition) the up-move appears to be gathering speed, in the US at least.

We have noted before that the background mood in equities seems to be slightly bearish as commentators point out how expensive valuations are at current levels or how very long this bull market has been in existence. It is very difficult for prices to start falling in the face of such bearish sentiment and so we will keep trying to find moments when prices will dip rather than trying to catch the eventual top of the move. That eventual high point will probably come within the next few months but bubbles can inflate fast and yesterday’s new highs in many US indices came with higher trading volume than in other days when new highs have been made – the market is poised for more. Be very careful when short-selling US equities from now on. We will advise as we get new signals.

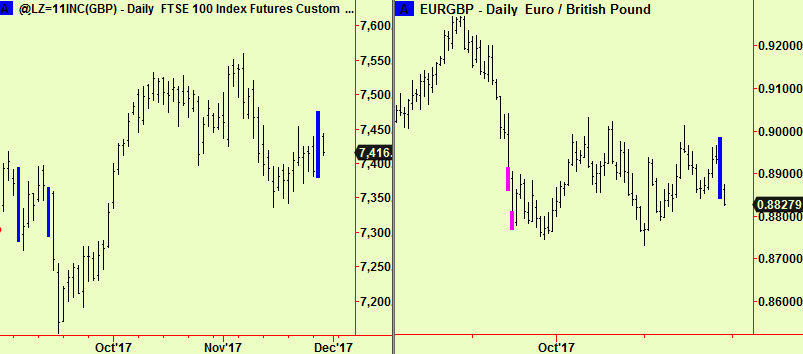

The situation is a little different in other parts of the world. European stocks have mostly not made much headway despite the US rally and there is a new compression in the UK’s FTSE index. Interestingly, there is also a compression in the £-Euro exchange rate:

These two markets have been sporadically linked since the Brexit vote – a weaker £ flatters the earnings of international companies listed in the UK so when there has been a correlation, it has been negative. The £/€ rate seems to be breaking its compression in favour of a stronger £/weaker € so far today which will provide an interesting test – if a stronger £ leaves the FTSE unshaken then it (the FTSE) will probably go higher. A more expected result would still be £ up, FTSE down. Watch for the break toward the end of the day.

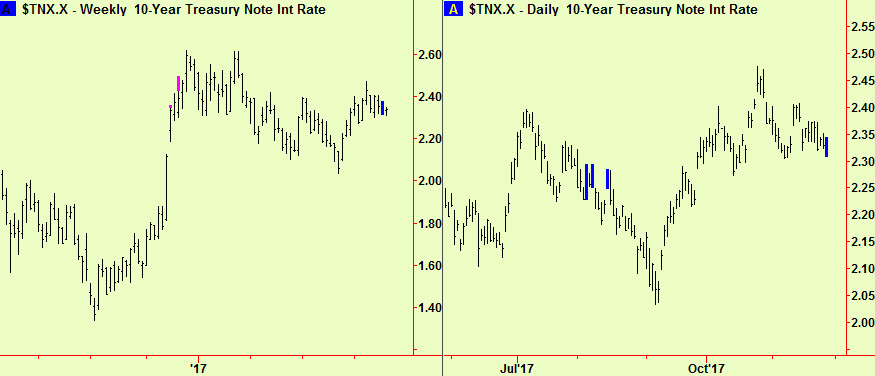

Elsewhere, US 10-year notes have compressed at both a daily and weekly scale:

These charts are both of yields, not prices which have also compressed but are not shown here. These signals come as no surprise after such a trendless period of ranging activity and argue that the market will soon start a new trend. In the face of (slowly) rising interest rates the logical inference is that the note and bond markets will fall, as we suggested in the November 16th edition but we prefer to wait for the break. European government bond markets had been a little firmer than these US instruments in recent weeks and have made several price top extensions in recent weeks. Those extensions are a bit old now, but they have not quite expired so they may provide a clue that the next move will be downward. We will soon see.

More soon, on commodities and currencies.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com