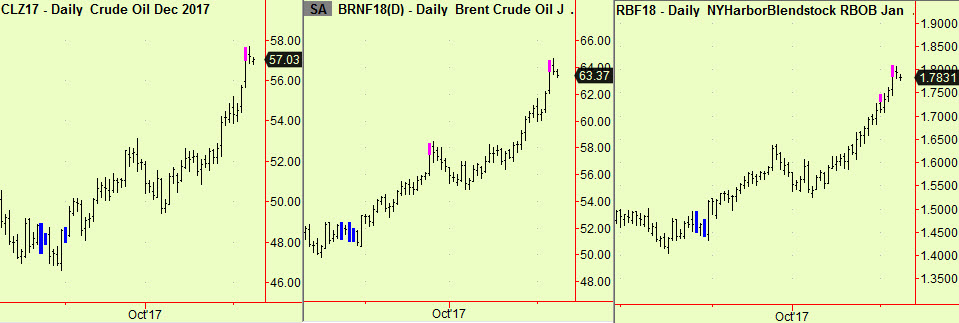

The weekend ‘night of the long knives‘ in Saudi Arabia has pushed up energy prices across the board. The alternate reasons are probably these:

- The ruling cabal of the current Crown Prince and his immediate supporters have purged their rivals using the (justified) excuse of corruption, copying Xi Jinping’s tactics in China. There is a lot more residual opposition in Saudi Arabia than there is in China however and the rivals who have been arrested or killed (two princes have died) are not unique. Saudi society has long been riven by dispute and rivalry at all levels – conspiracy is the normal state of affairs – and the outlook remains uncertain. Insurrection is unlikely but a palace counter-coup is possible. The most dangerous time is just after a revolution/putsch/ coup/purge when the dust has yet to settle. This opens the slight possibility of an interruption in oil supplies from a distracted Saudi Arabia.

- More likely is that the putsch will succeed and that the Crown Prince (together with his elderly father, the King) have indeed achieved their aim of consolidating power. This means that the likely result for oil supplies is that Saudi Arabia will continue to hold fast to the production cuts that it orchestrated throughout Opec and that the world’s inventories of oil will continue to diminish bit-by-bit. A further corollary of this unprecedented centralisation of power in one man’s hands is that the policy flip-flops that have already occurred on his watch will probably continue. Candid criticism is already rare in Arabian politics and this will cause it to vanish completely. It is possible to imagine a situation in the near future when Saudi Arabia opens the taps again and floods the world with crude to attempt some mixture of goals including:

- Discomforting its perpetual enemy Iran, with whom it has a proxy war in Yemen, next door.

- Trying once more to undermine American frackers (although this was a comprehensive failure last time it was tried)

- Rebuild the Saudi treasury, which according to some pessimists will run out of money as early as next year (we think they have five years more at present spending rates but others think there is less time)

None of this brings any certainty, which is why the oil market has pushed higher, but these are the relevant points that we think should be followed in the news for clues as the next weeks and months go by – after all energy is not truly a free market. In the meantime, crude oil has now extended, as has Rbob again. We covered shorts on the push to new highs but are looking for another point to sell. If we see one we will write it here but please choose your own trigger at any moment from now. Charts:

US Stocks have continued their dull range, with slight new highs in some indices every day or so. There has been a development that makes it worth attempting a short again – the Value Line broad index made a compression signal, as reported in one of the November 1st editions. It then made another four days later and that has now broken downward:

The second chart above shows a Russian equity ETF that has just made a compression that has broken in the opposite direction. If you can trade Russia, buy some for a ‘trade’ but we include this more as an illustration of the breakdown of global market forces that is occurring under present regimes around the world – markets won’t all move together for much longer.

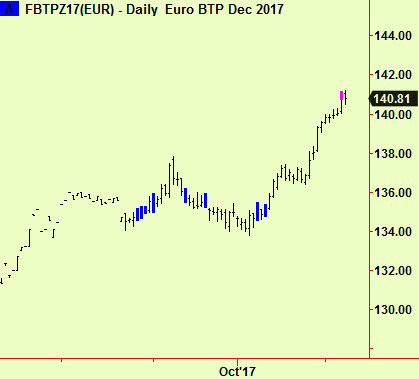

Elsewhere, the recent small global bond rally has now produced a top extension – in Italian government bonds:

As usual, we don’t take a top extension as an automatic sell signal – they usually indicate that a price rise is ending, not that a decline is about to start. We will be watching for reasons to sell this and other bond markets and we advise that you do the same.

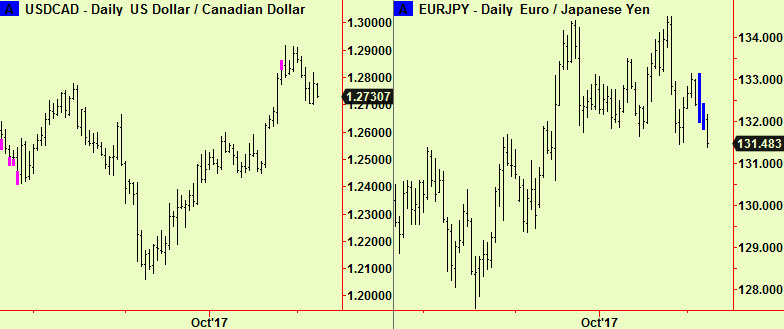

Lastly, we advised buying some currencies against the $ in another November 1st edition. One of the charts we showed was of the Canadian dollar (updated below) and there has since been a development in the Yen against the Euro, where a compression has formed and is now breaking in the direction of a stronger Yen:

This argues that:

- The $ has shown some signs of weakness beginning, so that a Canadian $ long position would now be in profit. Hold on.

- The Yen is showing signs of strength, so it too could be bought, but it might be better to buy it against the $ than against the Euro. Don’t wait, buy now.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com