The excitement overnight has been North Korea doing what they always do but even more so. Firing a rocket over Hokkaido is typical of the aggressive posture N Korea takes whenever anyone challenges them and should not worry the world unnecessarily – within the terms of their strange country their leadership acts rationally and this can only be understood if we remind ourselves that their only preoccupation is maintaining their grip on domestic power. The alternative is a wholesale massacre of the ruling elite and all their foreign encounters are designed to preserve current conditions – snarling at foreigners is not designed to provoke war but to show the N Korean people that the world is their enemy and their only protection is the Kim family. This is widely acknowledged in foreign policy circles – let us hope that someone in President Trump’s circle also knows it so that he may shrug it off as just more posturing.

Meanwhile, stocks have dipped a bit – enough to be bought again, as we recommended in the last edition. No-one can tell how big an event-driven market dip will be but we suspect that this one is likely to be small, which is why we began this piece with the commentary on North Korea.

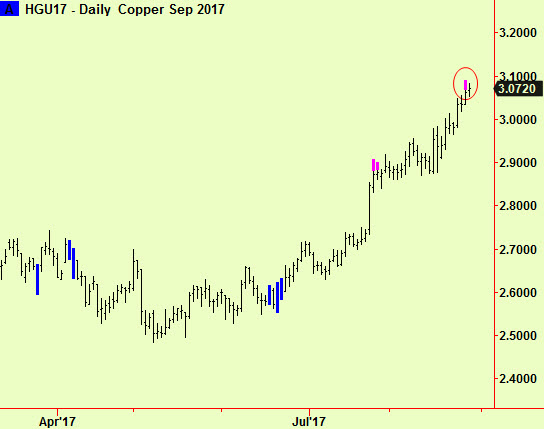

Meanwhile, copper prices have continue their upward march and have now extended at a daily scale (again):

The last extension was in late July and led to a ‘flat spot’ that lasted about three weeks. This is the normal shelf life for an extension and we expect that this new one will have effect for around the same period. We are still trying to find places to sell short and this new signal is a reason to concentrate harder. We usually don’t take a top extension as a cue to sell short immediately as such signals often mark the end of up-moves but not yet the start of down-moves – some ‘top’ may need to form before the price can weaken. If you have any longs, sell them now but we are not yet advising shorts unless you have some other reason, outside the scope of our analysis.

All signals courtesy of software supplied by our friends at Parallax Financial Research www.pfr.com