The immediate effect of the expected Trump administration tax changes are probably discounted – the so-called ‘Trump rally’ in stocks has been going on since the day after the election and part of the reason will have been the expectation of business-friendly initiatives such as this one. The prospect of a one-off tax break for US companies to repatriate large (untaxed) overseas cash piles from foreign sales is a different matter as the details will be vital so it is hard for markets to allow fully for the effects. Some consequences are guessable though, hence this edition.

One conclusion that was widely aired in the late weeks of last year was that both these changes would spark a flurry of mergers and acquisitions (M&A). The reasons are several but principally two – the ‘natural’ rate of acquisition of one company be another has been distorted by tax-driven overseas cash hoarding and that the cash involved has itself become so large that it represents an asset that might be bought at a discount if that company’s share price was too low.

There have been a number of tax-driven ‘inversions’ in recent years as a way for US corporations to navigate around the rules on repatriating profits, by arranging that they be bought by foreign-domiciled companies, many of which are nominally based in low-tax Ireland. The largest number of these have been in Pharmaceuticals (followed by Energy) and this is a strong clue that the next wave of M&A will also be in those sectors. Pharma is particularly fragmented compared with other vital parts of the economy and so consolidation is particularly likely in this sector.

Here we will not attempt to guess which the acquiring companies may be – that will depend on their individual fundamental outlook, including the attitude of the board and management, which we do not follow. We will try instead to identify which are targets, based on our style of analysis of crowd behaviour. If a stock seems ‘unloved’ but the brand is strong, we would guess that makes it a candidate. We start with Pharma and will deal with Energy in a later edition.

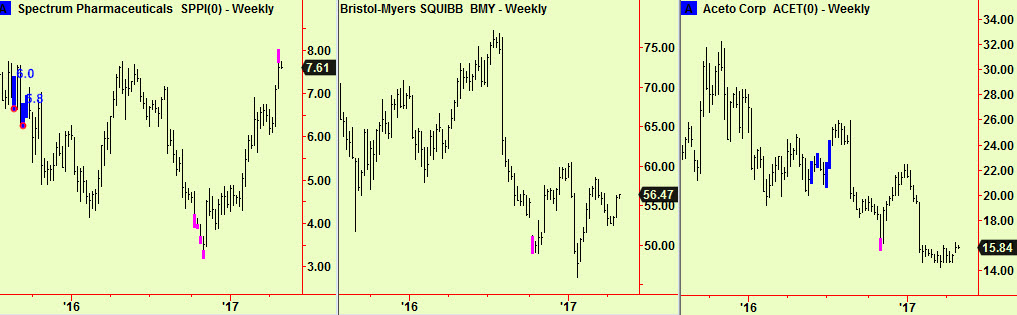

Of the fifteen major Pharma stocks in the lists we use (from TradeStation in this case) three have made weekly-scale bottom extensions in the past few months. This signal is our most reliable and indicates that the bearish mood in that stock has reached a crescendo – the very definition of unloved. They are:

Of these, Spectrum has already more than doubled and has made a weekly-scale top extension, so the situation is no longer attractive to buyers. Aceto bounced then dropped and it has shown no signs of strength since then but may be still be a candidate, although there is resistance at the level of the old compressions seen in this chart (in blue). Bristol-Myers Squibb has dipped twice since the bottom extension, and the most recent dip (in March/April) hardly dropped at all. This too is a candidate.

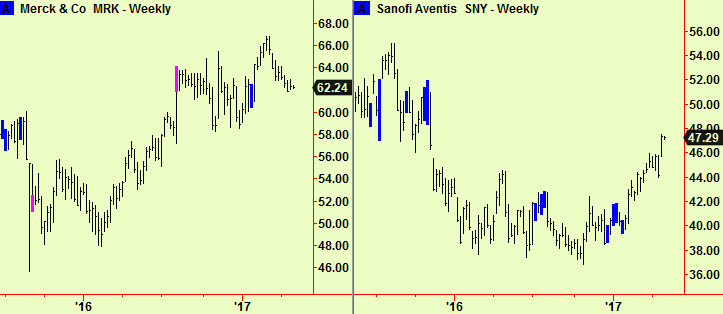

There have been two Pharma stocks that have moved up from weekly-scale compressions. These are also reliable signals, if a little less so than bottom extensions:

Of these two, Sanofi is a French-based firm which may reduce its attractiveness as a target for US corporations and the price is nudging up against resistance from old compressions late last year. This means it is not really a candidate, but Merck is – there is always support at the level of old compressions, when the price re-visits there and that is happening now.

So of the fifteen stocks in our list there are three candidates that we consider may benefit from any renewed enthusiasm for M&A in the Pharma sector – Merck, Bristol-Myers Squibb and Aceto. Aceto is relatively small and as mentioned, there is resistance nearby overhead, which reduces its appeal to our eyes, leaving only two. Merck is very large with a market cap of $170bn and has a huge cash pile (nearly $30bn, we think) which may make it indigestible to all but the biggest acquirer but Bristol-Myers Squibb is half that size and other analysts have already identified it as a target even though the price has not moved much. It also has lots of cash of course (a bit over $10bn) but this is probably not a deterrent. If we had to pick one, this would be it.

All signals generated by software supplied by our friends at Parallax Financial Research www.pfr.com