A well-known economist has just pronounced that US equities are over-valued. Perhaps this is newsworthy because the world’s most famous investor has also just opined that stocks still have value because interest rates (and bond yields) are low and likely to remain so – a simpler expression of what is sometimes called the ‘Fed model’ that compares yields on stocks with the ten-year treasury. A contest between the views of a Nobel prize winner vs the richest investor – which should we believe?

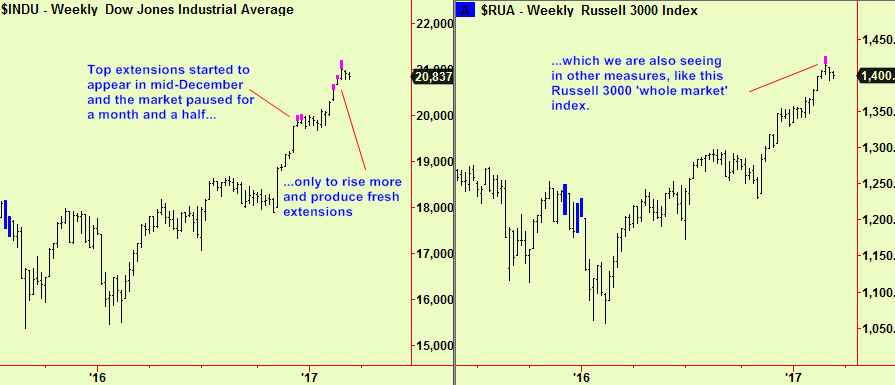

Our analysis has been showing that US stocks are over-stretched for some time. Our friends at Parallax Financial Research have a fundamental pricing model that shows that prices are 20% above ‘true value’ and we have also seen weekly-scale top extensions, starting late in 2016, which argue that the upmove should stall. These signals led to a ‘flat spot’ for a few weeks before prices rose again to their present levels. Now we are seeing more weekly-scale top extensions and the market has been trading sideways again:

This is typical of a bubble. Prices rise, the market pauses to ‘catch up’ with the new levels and then rises again, perhaps in a steeper trend. We have remarked on the likelihood of this long-term bull market since 2009 ending with such a bubble and it seems to be happening. It is important not to stand in the way of markets that have entered this stage, even though prices seem ‘stupidly’ high. The final stage of a bubble can mean prices rising in a few months by as much as the whole prior up-move, which can bankrupt early bears. See our January 10th edition for a picture of the Nasdaq during the 1999/2000 inflate-and-burst example.

It still seems unlikely to us that the whole market will inflate. If the driver really is the prospect of low interest rates for years to come then this is possible but it seems more probable that some sectors or groups of stocks will comprise the main bubble. Accordingly we have chosen the Nasdaq as being the most obvious contender, because of the prevalence of ‘growth’ stories in stocks listed there which have led to bubbles in the past. Tactically, we repeat the advice given on January 10th – ‘buy the Nasdaq on dips and sell the Dow or S&P on rallies.’

More later on European equities, where values are cheaper, but there are special risks.

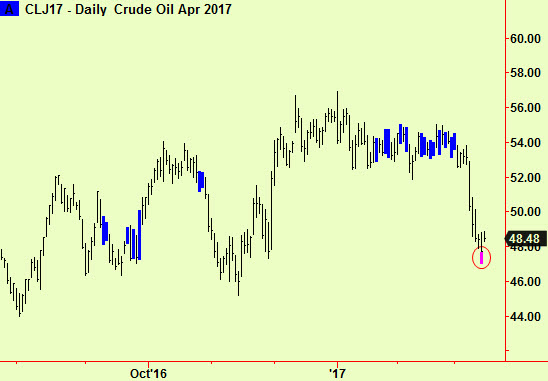

Meanwhile, the recent drop in Crude oil has led to a bottom extension in the front month WTI futures. This market is trading in a well-defined range/channel and we are now at the bottom end of it. Cover any energy shorts you may have taken based on our March 7th edition and start buying for a bounce. It would be sensible to try buying dips, but there may not be any…

All signals generated by software supplied by our friends at Parallax Financial Research www.pfr.com