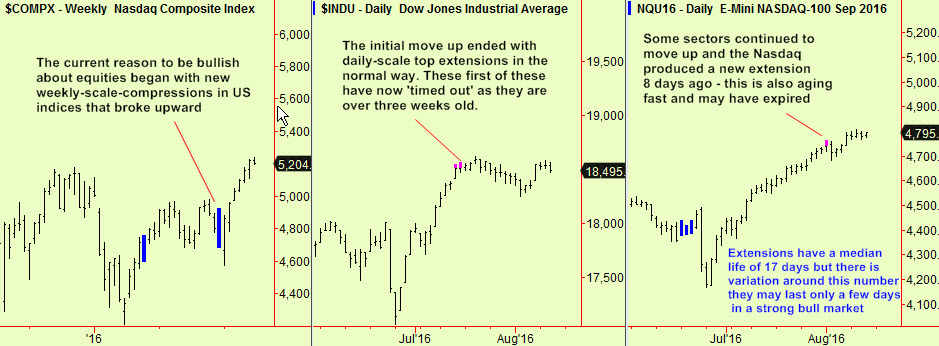

Stocks have generally firmed around the world during the last week. Those markets where uptrends already existed have made further gains and some of those that were in trading ranges have pushed above them. This fits our view that the next ‘leg’ up is under way and we have been trying to identify which market would benefit most from this new enthusiasm for stocks – see the July 26th edition for our ideas about candidates. We think that bubbles are likely to form as we enter the end-stage of this long-running US bull market. Some updates, showing how the main new US uptrend started with weekly compressions that broke upward, pausing after daily-scale top extensions that are now expiring:

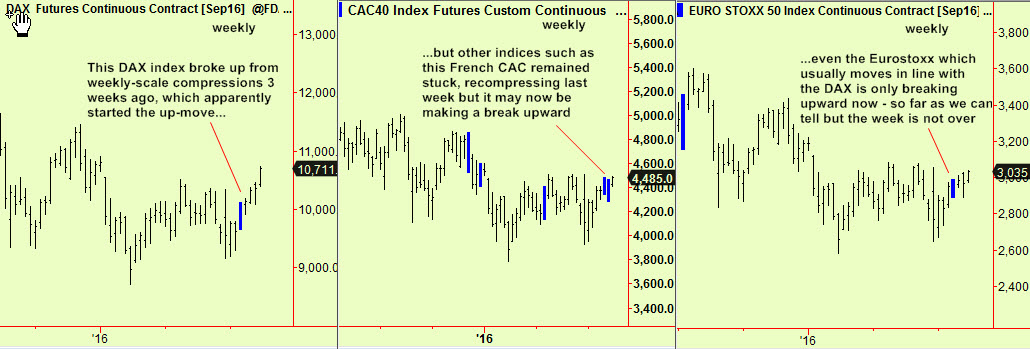

The situation in Europe has been a bit different. The long recession has harmed earnings growth and most national indices (and the Eurostoxx) have been stuck in trading ranges for years. That may now also be changing and it is worth pointing out that stocks are now much cheaper in Europe than in the US, when comparing like-for-like say Siemens vs GE for example. The long sideways range has produced some weekly-scale compressions in a variety of indices in Europe, the first of which to break was Germany. Now the others may be following so it is time to get ready to buy some more (if the break actually occurs, which we cannot tell until the end of the week, which is tomorrow). Brave hearts could anticipate and buy more now.

This divergent behaviour may contain a clue about what will happen next. The German market seems to have started its up-move already while these others are still waiting. This early start probably means that the Germany is a candidate when considering which markets may form bubbles in the months to come. The market cap of quoted German equities is surprisingly small compared to the size of the German economy because many of Germany’s larger companies are still private. That means a modest amount of fresh buying can move the index a long way up compared to the amount of buying that would be necessary to move US or UK markets an equivalent amount. The UK is probably also a candidate by-the-way but not because of signal readings such as these – there the reasons are more to do with the weakness of the £ and the consequent boost to earnings of the FTSE 100, 70% of which are denominated in other currencies. The prospects for UK growth are probably much better outside the EU too, regardless of the eventual details about what kind of departure will result from the negotiations that have not yet officially started.

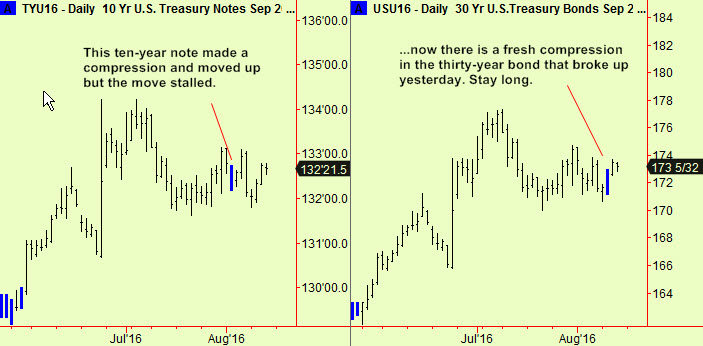

Elsewhere, Bonds have re-compressed. The compressions that we reported last week started to break upward but the move did not develop. Now, this new compression also seems to be breaking upward which is a reason to hold on to long positions.

More soon