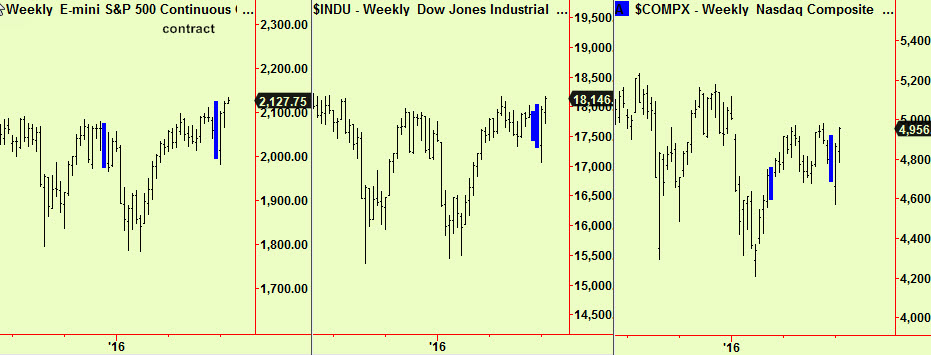

The warnings that we have been issuing since the end of the first quarter about a possible bubble in US stocks have suddenly become timely. There was a sharp dip in stocks everywhere after the pesky UK electorate rejected their superiors’ views and voted to leave. The rally that started from that low of that dip on the 27th June continues and has now pushed prices up above the level of compression signals that we reported in the July 1st edition. Here is a further update, showing that all three of these major indices have now pushed above those compressions:

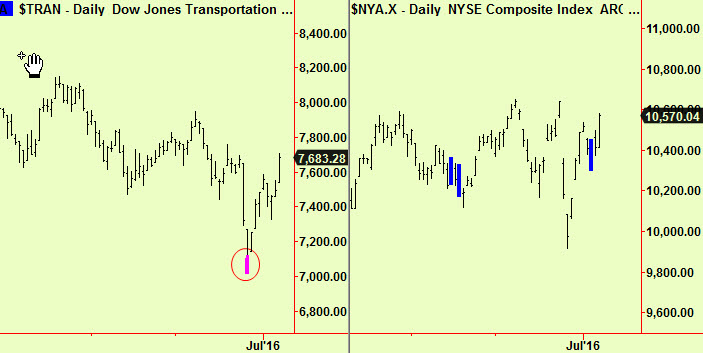

There have been some daily-scale signals that also point upwards. We reported daily-scale bottom extensions in some sector indices that marked the bottom of the move, including the transport index shown again here and there was a daily-scale compression in the New York Stock exchange composite on Wednesday last week that has since broken upward:

This all indicates that a new up-move is in progress in US stocks and by implication in other markets too. We have been expecting this break and so have been buying bits and pieces since Tuesday. There is probably plenty of time to ‘get on board’ for this move and so we advise buying dips as and when they occur if you are not already long.

There has been some commentary over the weekend that central banks may now over-react to Brexit and that this will result in ‘a stimulus too far’ and so a sharp rise in asset prices such as stocks and real estate (and bonds of course). We have made the same case in the past, usually calling this the ‘brick on a string’ situation but it is not the argument that we are using now. Both call for higher asset prices but the resemblance is superficial, so let me state our current case again: We think that a major change has occurred in the posture of the Federal Reserve – the US central bank. Previously the Fed has looked mainly at domestic US circumstances when deciding what to do in order to do its job – defined as aiming for “Maximum employment, stable prices, and moderate long-term interest rates.” The US economy is so large that it has been unnecessary to look much beyond its borders for things that would influence these aims and so the Fed’s focus has previously been domestic.

Globalisation has increased the rate of growth of international trade so exports now represent about a seventh of the US economy compared with a tenth only a few years ago. This is one reason why the Fed now looks outside the US for factors that could affect its task. So far, so unexceptional – this is what other central banks have always done. The US is a special case though – its economy is large and diverse enough that it has long had enough ‘critical mass’ to generate growth on its own and was always the ‘world’s locomotive’ that could pull the rest of us out of trouble. The Fed’s main job was to make sure this growth didn’t get out of control and cause a problem with inflation in boom times and to stimulate activity a bit when it faltered – usually because of Fed heavy-handedness in damping down demand in the prior upswing. This is the main cause of the ‘economic cycle’ so beloved of economists. It actually exists in the US whereas in other economies it is more just a useful concept and actual cycles are hard to identify. This is negative feedback in action between interacting two forces and it always tends to produce cycles – see our videos for more.

When a negative feedback loop is interrupted, any such cyclical stability it has produced is destroyed and strong new forces are unleashed. This happened with the creation of the Euro, causing the rise of Germany to be the world’s largest exporter and this shift in Fed focus could be just as serious. The world is not a happy place, economically speaking, and the current sorry state of affairs almost everywhere is likely to inhibit the Fed from raising rates at all. This can easily lead to a situation of headlong speculative rush into ‘hard’ assets, primarily stocks and real estate. US stocks have been trending higher since the lows of 2009 and when a mature bull market like this re-ignites then a bubble can easily form in which prices increase sharply, beyond all idea of ‘fair value’. Watch out.

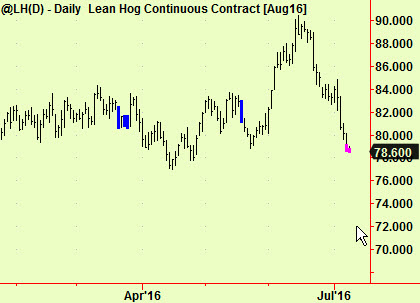

Elsewhere, there has been a bottom signal in Hogs, at a daily scale:

Buy some.