The markets reacted sharply to the news of a narrow win for the leave campaign in Thursday’s Brexit referendum here in the UK. Stocks fell everywhere; bonds, the dollar and gold all rose and fear now stalks the world. This is partly because the result was unexpected despite the close pre-referendum polling (Those Brits couldn’t really be so stupid, could they? etc.) and partly because this departure could act as a trigger for events far beyond the narrow point of whether the UK should be in the EU.

We will leave the political analysis to other commentators, except to say that free trade is widely seen as a good thing in Europe these days and particularly in Germany, whose voice should be loud when the negotiations of Britain’s departure are conducted. It seems unlikely that punitive retaliation from Europe against the UK will result and there will be some kind of trade deal. It is also a false conceit of politicians and diplomats that trade deals are necessary for there to be trade but of course this isn’t so. Nonetheless, there was enough prediction of disaster in the event of a vote to leave that the markets have indeed been fearful to the point of panic now that it has happened. Luckily the predictions of economists only serve to make those of astrologers look prescient.

The three main US indices all produced new weekly-scale compressions:

This means the obvious – these US markets are stuck in ranges that are yet to break in either direction. Earlier in the month it looked as though an uptrend had already started as previous weekly compressions broke upward – the last chart of the Nasdaq shows one of them. This uptrend has now stalled and we wait and see.

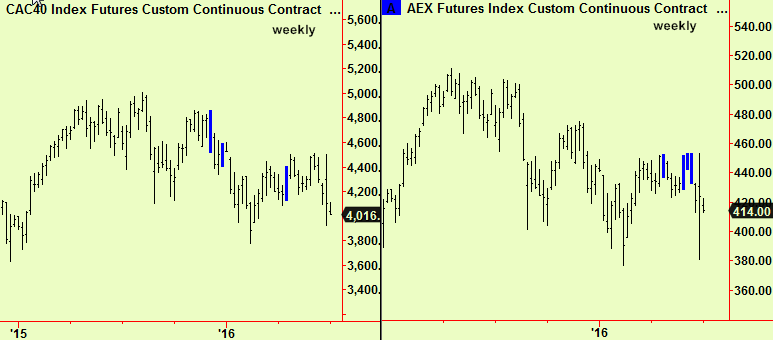

European stocks were much worse hit, as this is where the repercussions could be most serious. Every member state of the EU has a vocal anti-EU political party and some have good support. The fear is that more referendums could be called and so even the core EU (France Germany, Benelux, Italy) could start to fragment at a time where the adoption of the single Euro currency has already created great strain. There were no new signals in any of the major European markets and the most recent older signals are some weekly-scale compressions. Here are two examples, from France and Holland, both of which have clearly broken downward:

Scandinavian markets made new weekly-scale compressions, and both of these examples are trading below those levels today. With a whole week ahead, it is far too early to use this as a reason to become bearish here and now but it is a warning:

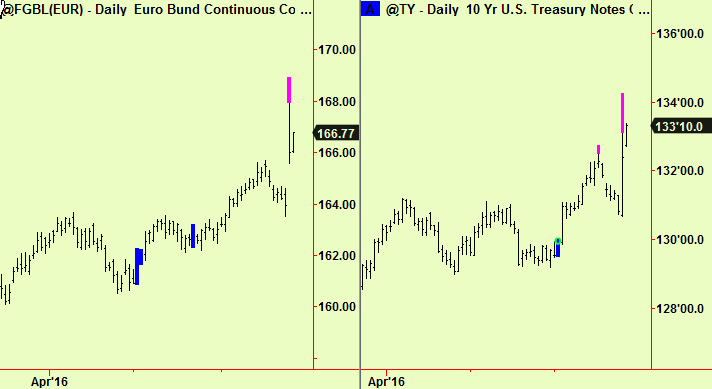

The ‘flight assets’ generally did make extensions, arguing that the rise was overdone. Bonds and 10-year US T-notes made top extensions:

So did gold, but the other metals were much quieter and copper even made a fresh weekly-scale compression:

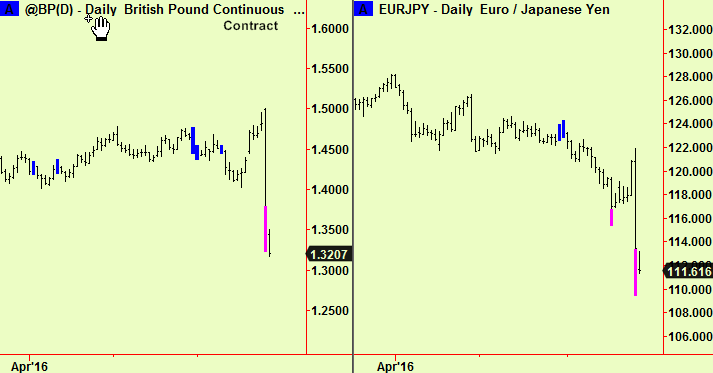

Currency markets also moved sharply, the £ being the weakest and the $ and Yen being the strongest. There were extension signals in cable, in the Euro-Yen and in $-Yen (not shown):

All this seems to indicate that the panic has been overdone. The extensions in Bunds, T-notes, Gold, the Yen and the £ show that these moves are at (or near) the end of their journey and that there will be some pause or snap-back shortly. The situation in Stocks is less easy, as compressed conditions can lead to a move in either direction and these new compressions reported in this edition cannot resolve until the close of the week.

Form a trading standpoint there are some arguments for buying US equity instruments, as they:

- were not nearly so badly ‘hit’ as the Europeans, so have demonstrated greater ‘resilience’ under pressure (so far)

- the various ‘flight assets’ have all made extensions as describe above, arguing that the panic is overdone

- US equity indices are still trading in a range that is roughly bounded by the trading on Friday – between just over 2100 and just under 2000 in the S&P futures. Prices now are 2001, which is near the low end.

It is also worth pointing out that some of the principal European indices have been falling since April (Germany and Eurostoxx) or May last year (UK and France). Bear markets often last for just a year or a little more and so it is reasonable to start looking for the end point and therefore a chance to buy. What better moment than when an anticipated and feared event has just occurred?

We will wait a bit, as there is at least the possibility that further general equity market weakness will develop – those new compressions make this a 50:50 bet. If weakness happens, it will probably weigh down on general sentiment and cause reduced activity in the real economy. It is well-known that the world’s central banks have empty arsenals with which to put up much of a fight if this happens and so the risks seem asymmetric – the rewards of an up-move in equities developing from hereabouts are outweighed by the risk of a sharp further drop. This should clarify within a few days and we will advise. If there is a further drop in equities, we would expect to see bottom extensions develop, which would be a signal to buy. We didn’t get any yet.