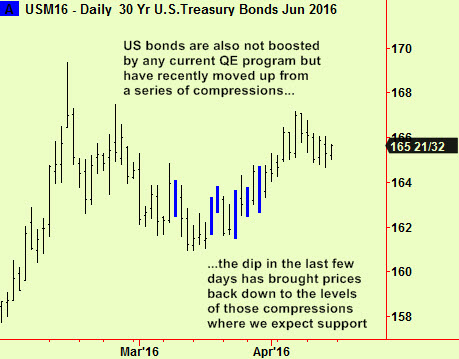

There were compressions in US 30-year government bond futures as reported in the April 6th edition. Prices moved up a bit and have now slipped back to the compressed levels where we expect to find support. Buy some.

We have been at pains to point out that any trading in bonds is more than usually risky. Short-selling has brought an end to several high-profile trading careers yet the artificial nature of the bull market causes every thinking participant to stop and worry that the enormous level of global debt cannot ever be repaid without bond investors sharing eventually in some large losses. Nonetheless, we keep dancing but with one eye on the door.

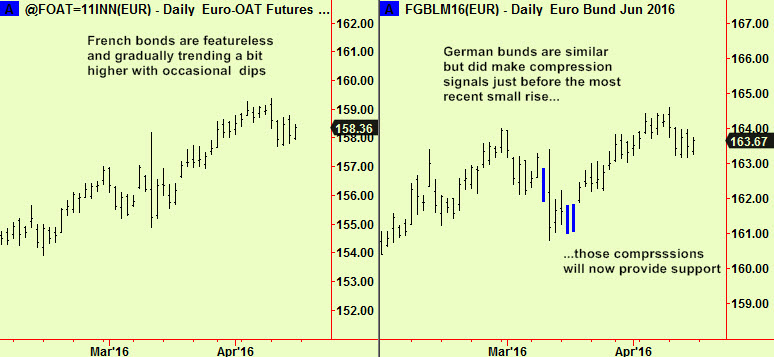

In Europe there is still QE in the Eurozone but not in the UK and other non-Euro members. This difference can been seen in the bonds issued by the different member countries. The big two in the Eurozone are France and Germany and their bonds have moved in lock-step, despite their different economic situations:

These two will probably continue to creep higher and we may advise buying dips, even though the upside potential is (probably) quite limited – yields are already sub-zero for the first few years of the yield curve. There may be enormous trouble ahead though and investors may even be prepared to endure yields that are even more negative than now and that may become negative for even further maturities, in the hope that these governments will default last.

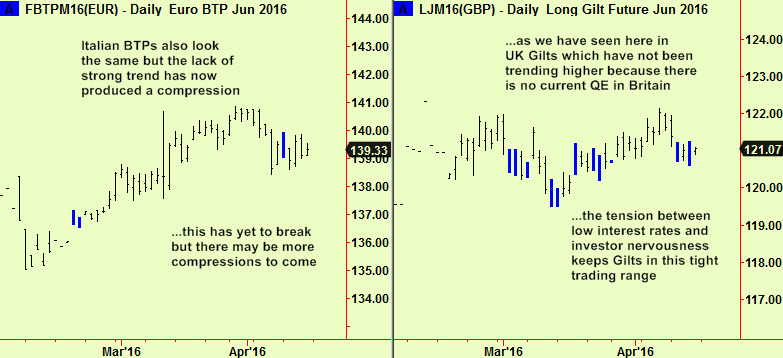

The contrast between a QE jurisdiction and one that doesn’t have it can be seen in Italian and British government bonds. Italian BTPs have a gradual uptrend just like OATs and Bunds but Gilts have traded flat for many weeks.

Again, we must assume that the gradual uptrend is still in place for BTPs and the recent compression hows that there may well be another move up in the near future – of course we cannot predict the direction of a compression break in most markets but these Eurozone bonds are ‘managed’ at the moment so the odds are distorted in favour of a continued uptrend. Gilts may also move higher, following their US cousins but we would stay out for now, even if the latest compression seems to break upward – the danger of a false break followed by further compressions is too high.

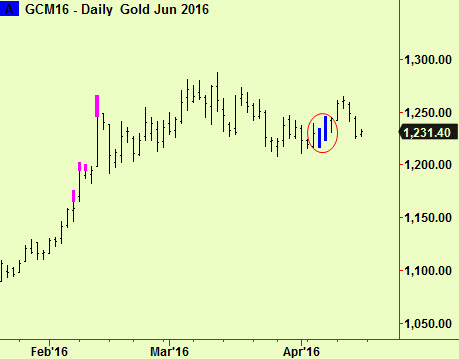

Lastly, more on gold. Futures compressed and apparently broke higher last week, as circled in the chart. The move stalled after a day and a half and prices have now dropped back into the compressed area:

This is where we expect to find support, as usual in these circumstances (see bonds at the top of the page). Prices have dipped quite deep into that support already so we must point out that there is a risk that the support will not hold. If prices drop through the lows of Wednesday 6th April ($1217.20 in June futures) and close below that level then we will become bearish. For now we are slightly bullish.