A sharp two-day drop in Chinese stock markets is being blamed for the general weakness that has gripped world equity markets in the first trading days of 2016. This is surprising as China’s equity markets have usually ‘gone their own way’ being largely unaffected by outside markets nor having much effect on them – perhaps this new connection is the real sign of China’s inclusion in the economic world order. There is likely to be some pause in the descent of Chinese stocks, as shown in the charts later. First some comments.

The authorities in China have been attempting to inhibit market weakness during the drop by restricting the selling activity of some of the institutions that they control (they influence all of them but directly control some too) and reportedly by also entering the market as a buyer of equity instruments as part of this ‘support operation’. Market control has a messy and largely futile history and this is unlikely to work for more than a short time if we are to compare this with previous attempts. Some examples:

Japanese governments began to act as a player in the bull market of the 1980s, acting to ‘punish’ short sellers by organising ‘squeezes’ when shorts had identified some over-valued share or sector and taken negative positions. These were directly attacked with the policy aim of didsouraging such unpatriotic activity in the future and contributed greatly to the bubble that inflated and eventually burst there in 1990, leaving the economy hollowed out and still suffering today, a quarter-century later.

Commodity markets experienced several booms and busts in the 1970s and 1980s. There were genuine supply disruptions behind some of the rises in price but there was a general mania too and some markets went up merely because others were rising. Oil had tripled in price and inflation was rampant so there was a willingness to buy all commodities with very little encouragement. There was also an expectation that some central authority would try to ‘dampen’ excessive price movement by the use of rules and market activity – buying to build ‘buffer stocks’ when supply was generous and selling from these stocks when demand exceeded supply, fro example. All these ceiling price/floor price schemes went bust or were wound up eventually.

With that background, in the mid-1970s the cocoa market governing body decided that there was a great deal of speculative ‘long’ accumulation behind a considerable rise in London cocoa prices and so changed the margin rules one afternoon. Any large long position must immediately post margin of £10,000 per contract compared with the roughly £1,000 needed until then. Prices fell by around 20% in an hour or so but had completely recovered all the lost ground by the close that day.

In contrast, the authorities in charge of the main precious metal exchange in New York (Comex) during the silver bubble of the late 1970s managed to end the market’s rise by a similar manoeuvre in March 1980. Here the margin requirements, position limits and the amounts that any one trader could demand be delivered were altered suddenly and the market collapsed 50% in 4 days, never recovering and then falling much more. In both these cocoa and silver examples there were allegations that insiders had taken short positions just before these rule changes, implying that the authorities were not just interested in the outcome, as they should be but also personally involved, which is hardly laudable.

Also in contrast, the oil cartel OPEC managed to control the price of oil in favour of (high) stable prices for several decades after the initial price rise that created the organisation’s power in 1973. This was remarkable considering the wild swings from glut to shortage that had always prevailed before (and do again now) in the oil trade and was largely achieved by Saudi Arabia acting as the ‘swing producer’ – reducing output in times of surplus and increasing it in times of plenty. They forgot this lately it seems, trying instead to bankrupt emerging producers by over-pumping. Silly Saudis.

This random selection of examples illustrates one point – it is extremely difficult to manipulate markets for more than short periods and the bigger the market the harder it is to do so. The Chinese stock market is small related to the enormous size of the economy but it is still worth almost $7 trillion (down from $10 trillion at the height of enthusiasm in June last year). This is extremely hard to control even in a country that still has ambitions to ‘command and control’ its economic activity. As a Vietnamese official revealingly asked a western visitor some years ago ‘We would like to have a free-market economy. How do we plan one?’ You can’t, came the reply.

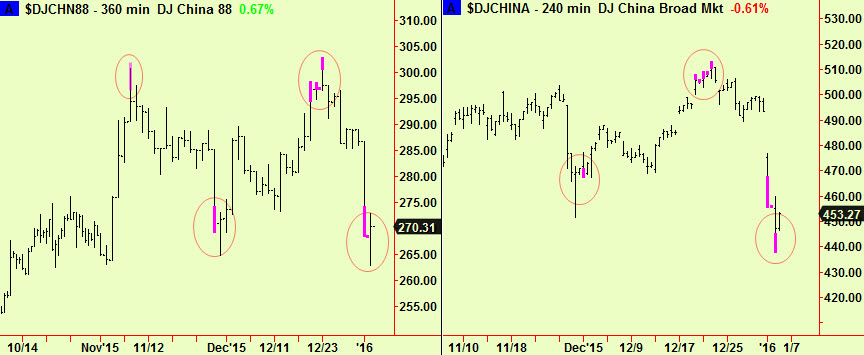

As to the Chinese market now – the drop has only lasted two days which is not enough time for our methods to generate a bottom extension at even a daily scale. We are seeing multi-hour extensions however, which have a good predictive record in China:

By their nature, these intra-day signals have a shorter shelf-life than daily, weekly or monthly signals but this still indicates that the drop has probably ended for the next few days or so which could allow other markets to experience a relief rally. In the longer-term the prospects for a bigger recovery in Chinese equities seem distant – the market’s worries obviously need more purging and the authorities are only postponing that reckoning and maybe making it worse.