The excitement of the pointless Greek referendum has come and gone, bringing some weakness to equity markets but more to commodities. That vote marked a new low in the posturing that has been a feature on both sides of these negotiations between the chronically indebted Greeks and their mainly European creditors. We have refrained from commenting much on the current Greek debacle but our long-term readers will know that we first pointed out that establishing a single currency that roped highly productive economic regions together with weaker ones would exaggerate their differences back in 1996. It was not possible to see that the winner would be Germany then, as the reforms that transformed it from the ‘sick man of Europe’ (yes, really) into the world’s greatest exporter were still seven years in the future but it was apparent that there would be winners and losers and this would depend on productivity levels.

After the ‘Hartz plan’ began in 2003 to loosen the labour market rigidity that was throttling Germany, productivity improved steadily there and the resultant accelerating economic performance was not hindered by a rising currency or rising interest rates. German exports began to climb and the less-productive European countries also benefitted from the general boom. Only when the banking crisis began in 2007 was it apparent that the Southern-Europeans (and Ireland) had merely been borrowing to spend and their prosperity was a cruel illusion. The productivity gap between Germany and the South continued to widen and there was no chance of enacting proper (German-style) reforms in the middle of recession so the result was and is, widespread unemployment in the Mediterranean countries, full employment in Germany and massive migration in search of work.

Obviously Greece is to blame for borrowing too much but the real fault lies in the existence of the Euro itself. When economic collapse occurs, no government finds it easy to cut expenditure and the relentless election cycle means there is always a political populist ready to claim that they have a painless answer in order to gain office. So now we are at the end of this game in Greece at least but the posturing hasn’t finished. There is an explicit threat that Greece must pay or leave the Euro, despite this being a completely invented rule. If America had a government of grown-ups, this would have been solved by now with some hard pressure from the White House on Greece’s creditors to reach a solution under threat of serious consequences. Greece can’t pay, as everyone knows, so why get tough now? Greece should not want to remain in this straitjacket of course but their pride would be hurt by leaving. The best thing is for them to get over it and walk away as soon as they can steel themselves to do so.

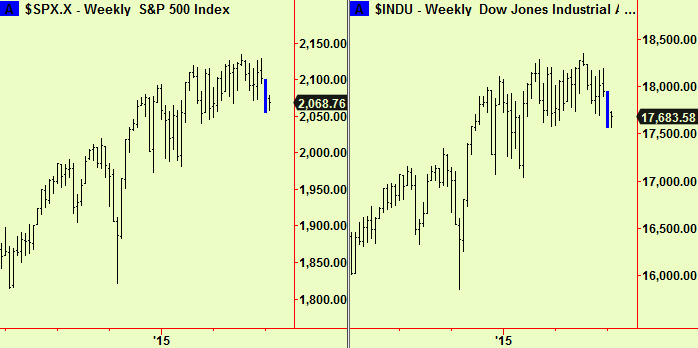

Meanwhile US equity prices dipped in very early futures trading on Sunday. We have a policy of only keeping protective stops in markets when they are liquid enough that one or two big orders won’t push prices around in thin conditions – without this our S&P sell-stop would have been elected on the low prices that were made on that early opening, from which prices then climbed all day. This is important because there are fresh US equity index compressions at a weekly scale to deal with:

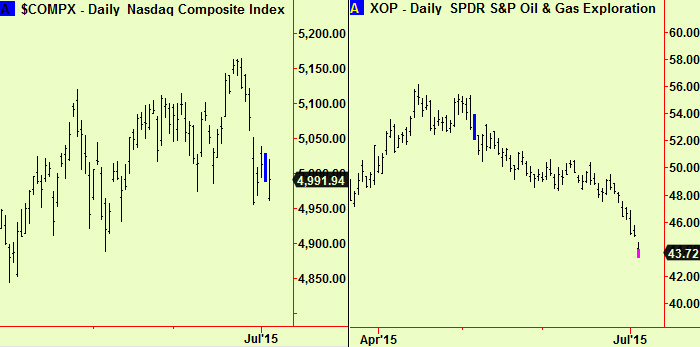

There were many of these new compressions in the US last week, so these two are just examples. A break in either direction will probably mean a new trend in the direction of the break but this will only become apparent nearer the end of the week – possibly not until the last day. For now, we sit nervously long with the same protective stops in place as before – see the June 18th edition for details. This compressed condition was confirmed by a daily-scale version in the Nasdaq composite on Friday, which wasn’t broken at the close yesterday, despite the day’s wide price range. There was another interesting signal however – a bottom extension in an oil and gas exploration SPDR which we would now buy. The US equity portion of our portfolio has no extra room in it to do so but we advised a short position in crude oil futures in the June 26th edition. We are already looking to cover this in whole or in part in the next few days, as it crossed the profit-taking threshold on Friday and this bottom extension in a related instrument is another reason to do so. Charts:

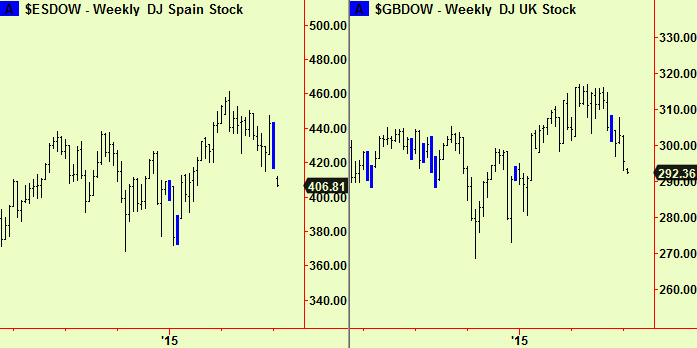

Equity prices also fell in Europe and have stayed relatively weak. We were stopped out of our long Eurostoxx position and don’t see a reason to take any new equity index positions in Europe for now. There have been weekly-scale compressions here too, in the UK 4 weeks ago and Spain last week, but we want to wait until nearer the end of the week before taking action – Spain has started to break downward but it is too early in the week to take this as a sell signal yet and the UK is back in support from an older compression:

None of this has had much effect in Asia where the main focus is the sharp drop in Chinese stocks and the authorities’ attempts to halt this tide. If we had any doubts that the bull market in China is over, they would be removed by this ham-fisted activity that only serves to highlight the difficulties of pretending still to be a communist country while actually running a kind of ‘crony capitalism’. Markets are a force of nature and when unleashed will not be denied. We have recommended a long position in China just for a ‘trade’ and we expect to be out of it very soon.

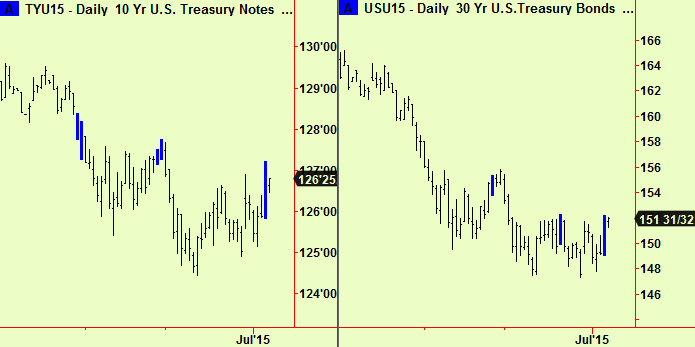

US 30-year bonds have also just compressed, as have 10-year notes. This reinforces the general ‘knife-edge’ situation that all these important capital markets have entered and we expect more fireworks soon. Don’t forget that compressions can break either way but they also presage an increase in volatility…