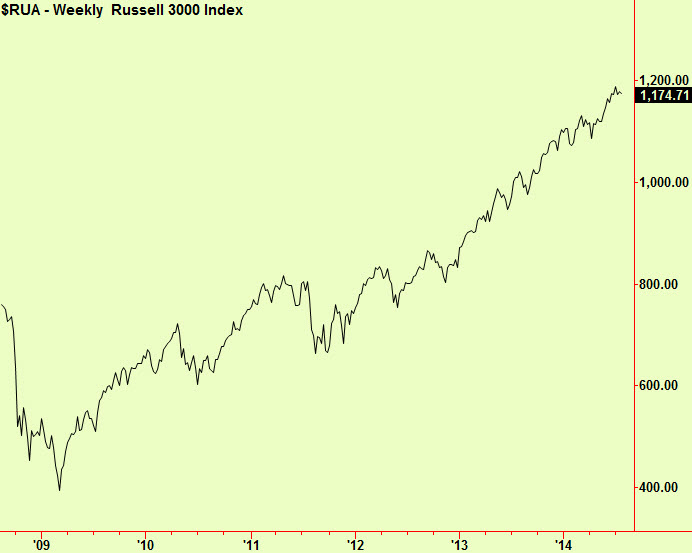

US equities have been moving higher since a major low point in 2009. Since the middle of 2012 the uptrend has been getting progressively smoother as the up-and-down wiggles have diminished in size, quarter by quarter and have also become more frequent. In recent months the trend has also steepened a bit and these features are visible in the first chart, a weekly-scale view of the Russell 3000, that includes most of the quoted stocks in the US:

A smoother and steeper uptrend with faster fluctuations is a sign that a bull market has entered its final phase. We look for this same behaviour in our Hurst-based indicators (see our movies on www.hedcapital.com for an explanation of our methods) and on rare occasions it can be seen with the naked eye, as pointed out by Didier Sornette in his books.

Earlier this year our analysis began to warn that there was some danger of a drop as we started to see monthly-scale top extensions. These are too vague for timing but they do warn of trouble ahead and prices dipped a bit. In May, weekly-scale compressions appeared that soon broke upward – indicating that another ‘leg’ up was in progress, so the danger was postponed:

This fresh strength doesn’t mean that we ignore the longer-term warning signals, but the ‘last gasp’ rally has to finish before the process comes to a final end.

There are signs that this rally is under way as the upward break of weekly compressions was followed by a dip back toward the levels of those compressions, where we expect to find support. These ‘return to compression’ movements are valuable as they give a second chance to enter a trending market if you missed the initial break. The bigger parts of the trend are usually still to come at such moments.

It is entirely possible that the trend will continue to steepen so that this next (probably last) leg up may be quick and big. The dangers of trying to catch such a move are obvious but investment clients are unforgiving if their manager prudently steps aside in these late stages – we will advise when we think the whole bull run is ending so that you can try to catch these last profits on the long side with reduced risk. We have not yet advised a new long position in US markets and we are watching for an opportunity to issue one.

The implications for other equity markets are mixed, but obviously a strong US market could have bullish effects around the world, despite the country’s diminished status in recent years. Europe will probably also rally if the US does and may of course accelerate upwards if the ECB is persuaded to embark on some version of QE. As ever, we prefer the equity markets of Germany and its close economic relations as prospects for the long side, for reasons often given – we already have an outstanding long recommendation in Germany and the Eurostoxx.

China is compressed at a weekly scale – not for the first time in recent months – and we wait for a break, which may be occurring this week. This could still go either way however and the general lack enthusiasm for Chinese stocks has puzzled those who think that economic growth is always connected to stock market performance. Surely even 7.5% growth warrants a lively bull market? No it doesn’t, so we wait for a confirmed break.

Korea has just moved up from a weekly-scale compression too and can be bought, probably even ‘at market’ as it hasn’t yet moved far. Watch out for some later dip back down to the compressed area however, as is normal. Return movements are not inevitable and sometimes a compression break lead to a ‘runaway’ move, so we always try to catch the initial break.

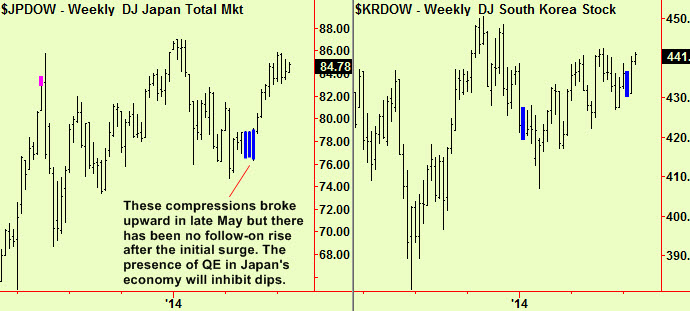

Japan is in the middle of a full-blooded stimulus exercise with quite small results so far from the stock market. There has been a modest move up from weekly-scale compressions in early June, so the market has begun an up-trend, even though it is not showing any recent strength. The presence of aggressive intervention in the Japanese market has probably stopped the market from having any dip and this will probably continue, so the risks of buying now and then seeing a dip begin are not too severe.

What this means for bonds: there have been top extensions in Bunds at both daily and weekly scale recently and we would short-sell here:

This is a change of view for us, as we have been broadly bullish and looking for a place to re-establish long positions until these weekly-scale top extensions came along. There may be similar reasons to sell other bonds soon—we are watching closely.